Confused between IBAN and SWIFT? Learn the key differences, how each is used, and when to use them for global bank transfers.

IBAN vs SWIFT: The Complete Overview Of International Banking Codes Relevant For Cross-Border Transfers

Imagine this: you are trying to transfer money to your cousin studying in Germany, and now you are faced with banking codes like SWIFT, BIC, and IBAN. As if reading ancient hieroglyphs. Do not worry, I have also been in such a situation, and that is the reason I am here to explain all that is necessary regarding the difference between IBAN and SWIFT codes in simple words.

Having guided many friends through international transfers for the first time, I realized how frustrating understanding these codes can be, especially when they are often seen as helpful and quite essential for saving both money and time. Allow me to show you everything in systematic order.

What Are International Banking Codes And Why Should They Matter To You?

Consider these as the same as a postal address, but in the context of money. There is no way to send money without having this code, and similarly, sending money without having banking identifiers is impossible. All your hard-earned money will not land in a random account; instead of using a random set of codes you came up with.

Here is what underpins their importance:

- They assist in avoiding expensive transfer mistakes and stoppages

- They enable banks to meet international compliance

- They aid in the optimization of the entire cross-border payment service

- They minimize payment fraud and increase the security level

The two main players in this game are IBAN (International Bank Account Number) and SWIFT codes. While both serve the international banking ecosystem, they have completely different purposes, and that’s where most people get confused.

IBAN Explained: Your Complete Account Identifier

What Is an IBAN Code Precisely?

An IBAN is essentially your bank account number on steroids. Unlike your ordinary account number, which is valid only within borders, an IBAN is meant to be global. It is like shifting from a local to an international phone number – all of a sudden, you are accessible to everyone.

The IBAN system arose in Europe during the 1990s when banks were trying to find a way to efficiently manage payments across borders. Presently, more than eighty countries, mostly from Europe, the Middle East, and certain regions in Africa and Asia, use IBAN.

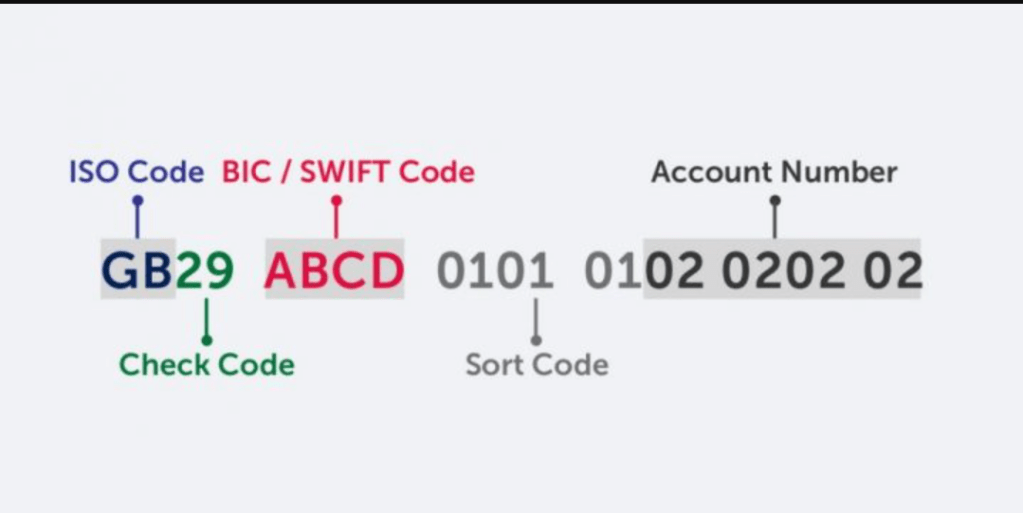

Dissecting the IBAN Format

Like many codes used internationally, IBANs have a systematic structure that is logical to follow. I can illustrate this with an example.

Sample German IBAN: DE89 3704 0044 0532 0130 00

Let’s break it down:

- DE = Participating country (Germany)

- 89 = Validation and control number

- 37040044 = Issuing bank (sort code)

- 0532013000 = Serial number or account number

The remarkable feature of this system is that it enables reliable fault detection. The aforementioned control digits aren’t random; rather, they employ a mathematical method that detects roughly 97% of errors. This minimizes the number of attempts needed to transfer money and reduces the chances of being stranded in a banking void.

Country Differences in IBAN Lengths

The rest of the world pales in comparison to the length of the IBAN code some countries use. While the lowest stands at 15 characters, some countries stretch it to 34. Here’s a side-by-side comparison.

| Country | IBAN Length | Example |

|---|---|---|

| Norway | 15 characters | NO93 8601 1117 947 |

| Germany | 22 characters | DE89 3704 0044 0532 0130 00 |

| Malta | 31 characters | MT84 MALT 0110 0001 2345 MTLC AST0 01S |

This discrepancy exists attributed to different domestic banking system structures within various countries.

SWIFT Codes: Identifier of Global Network Banking System

An Overview Of SWIFT Code

As mentioned in the previous section, People commonly refer to SWIFT codes as the Society for Worldwide Interbank Financial Telecommunication network. Apart from being merely a coding, it is indeed a secure telecommunication network that interlinks more than eleven thousand banks from two hundred countries.

SWIFT processes more than forty-two million messages and transactions on a daily basis, which adds up to trillions of dollars. It’s essentially the internet of international business banking, and in this scenario, SWIFT codes are equivalent to the addresses that validate the entire process.

Explaining The Construction of SWIFT Code

Similar to BIC codes, SWIFT codes are equally crucial as they are shorter than IBANs. Just like IBANs, they too stand to post 8 and 11 characters.

Example: DEUTDEFF500

- DEUT = Bank code (Deutsche Bank)

- DE = Country code (Germany)

- FF = Location code (Frankfurt)

- 500 = Branch code (optional)

In this case, the branch code is optional; in case it’s absent, the SWIFT code denotes the main office of the bank. This characteristic aids International Transfers; Payment SWIFT codes are very supportive.

BIC vs SWIFT: Clearing up the confusion

This is incorrect and has gathered a lot of concern around it. BIC (Bank Identifier Code) and the SWIFT code are the same. Both do exist interchangeably in the everyday working of the banking industry, but it is safe to declare that “SWIFT code” is what most commoners prefer.

“Elevator” and “lift” both refer to the same concept, but have different terminology.

IBAN vs SWIFT: The Ultimate Head-to-Head Comparison

Understanding when to use IBAN or SWIFT will depend on understanding the very basic difference between them. Let’s dive into it.

| Feature | IBAN | SWIFT |

|---|---|---|

| Primary Purpose | Identifies your specific account | Identifies the bank location |

| Length | 15-34 characters | 8-11 characters |

| Geographic Coverage | 80+ countries (Europe-focused) | 200+ countries worldwide |

| What It Contains | Complete account information | Bank and location details only |

| Usage Context | European/SEPA transfers | Global wire transfers |

| Typical Fees | €0-5 within the SEPA zone | $15-50+ for international wires |

| Processing Speed | Same day (SEPA) | 1-5 business days |

| Error Prevention | Built-in validation | Manual verification needed |

The Key Difference That Changes Everything

The big difference is that IBAN tells you where the money should go (the account), while SWIFT tells you how to get there (through which bank).

For example, imagine sending a package overseas. The SWIFT is the routing information for the postal service; it gets the item to the correct postal facility. The rest of the address is the IBAN, telling the local worker the exact house where the package should be handed over.

Real-World Scenarios: When to Use Each Code

European Transfers: IBAN’s Home Turf

Last year, I transferred money to my friend in Amsterdam; all I required was her IBAN. The rest was done through SEPA. Within the confines of the SEPA zone, IBAN holds dominion for several reasons:

- Transfers are processed as domestic payments

- Fees are typically minimal (often free)

- Processing happens same-day or next-day

- No currency conversion within the Eurozone

Located within 36 countries, the SEPA zone includes all EU member states, as well as Iceland, Norway, Switzerland, among others.

SWIFT network vs IBAN system: Global Transfers: SWIFT’s Domain

The story changes when I need to send money to my cousin in Japan. As I mentioned earlier, Japan does not use IBAN; therefore, I require:

- The bank’s SWIFT code

- The complete account number

- Additional routing information

This is where knowing the difference between the SWIFT network and vs IBAN system comes in handy. SWIFT deals with international messaging, while correspondent banks deal with international funds transfers.

Do I Need Both IBAN And SWIFT?

This is likely to be the first question that comes to mind for most people. The answer revolves around the destination of the funds:

Within SEPA Zone:

- IBAN only ✓

- SWIFT optional (but helpful)

To Non-IBAN Countries:

- SWIFT code required ✓

- Local account number required ✓

- Sometimes routing codes are needed ✓

From Non-IBAN to IBAN Countries:

- Both codes are often requested ✓

- Ensures fastest processing ✓

Cost Analysis: Your Money Matters

Understanding the IBAN vs SWIFT pros and cons from a cost perspective can help you a great deal. Let’s clarify what the fees are:

Expenses Linked To IBAN Transfers

SEPA Payments (within Europe):

- Most banks: €0-2 per transfer

- Online banks: Often completely free

- Currency conversion: Mid-market rates

Non-SEPA IBAN Transfers:

- Traditional banks: €15-25

- Online services: €3-8

- Currency margins: 0.5-4%

SWIFT Wire Transfer Expenses

The Hidden Cost Structure:

- Your bank’s fee: $15-50

- Correspondent bank fees: $10-30

- Receiving bank charges: $5-25

- Currency conversion markup: 2-5%

I learned this the hard way when what I thought was a $25 transfer ended up costing me close to $80 in total fees. Never estimate the total until you’ve gathered all the information first.

Security and Compliance: How Your Money is Protected

While both IBAN and SWIFT in international transfers have protocols to offer, both differ in the protection measures they offer:

IBAN Security Features

For IBANs, human error is mostly eliminated through the check digit algorithm. Think about it as a spell-check on bank account digits. Of course, this does nothing to prevent chaos caused by intentional fraud.

SWIFT Network Security

SWIFT protocols have different hierarchically placed encryption and authentication safeguards for each type of communication. These include:

- Message authentication codes to verify the sender’s identity

- End-to-end encryption for all communications

- Suspicious pattern real-time alerts

The Most Costly Incorrect Actions

With over 10 years of helping people with international transfers, these are the most common errors I see:

IBAN Mistakes

These are errors made with international bank accounts and are the most common:

- Space duplication: Most people do not realize that IBAN formatting requires the inclusion of spaces

- Character usage: Confusing O with 0 or I with 1

- Using old information: Old IBAN data is a common issue for most customers

Pro Tip: Before any international transaction, every user is advised to check if their bank provides IBAN validators and generators.

SWIFT Code Errors

Common Issues:

- Employing obsolete SWIFT codes (these are periodically updated by banks)

- Neglecting to include branch codes where necessary

- Mixing up closely related bank codes

How IBAN and SWIFT Work Together

Receive it all: these are codes that, far from competing with each other, are in many cases used interchangeably alongside one another. For most international transactions, both will be needed:

- SWIFT code directs your transfer to the right bank

- IBAN guarantees the funds are directed to the proper account within that bank

- Correspondent banks facilitate the actual movement of funds

This collaboration becomes critical for sophisticated routing, like sending a payment from the US to a tiny bank in Europe.

Resources to Consider Prior To Your Next International Transfer

How to Transfer Money Online – The Most Efficient Ways

I have listed the most efficient ways for bank money transfer in my experience:

For IBAN Transfers:

- Utilize IBAN checking tools for validation

- Look into SEPA exemptions for lower pricing

- Wise or Remitly can be cost-efficient alternatives

For SWIFT Transfers:

- Validate the SWIFT codes using authoritative sources

- Evaluate all-inclusive pricing across all competitors

- Look at bank transfer services for better options

Primary Cross-Validation Tools

IBAN Validators:

- Your bank (most trusted source)

- IBAN.com (offers an extensive database)

- European Central Bank validator

SWIFT Code Directories:

- SWIFT.com official registry

- TheSwiftCodes.com (simple interface)

- Your bank

International Bank Account Numbers and SWIFT Codes: Their Future Developments

With time, the picture will be completely different. The outdated systems are gradually being replaced with ISO 20022 messaging standards, which allow for more detailed shippable packages throughout the globe. At the same time, Central Bank Digital Currencies (CBDCs), cross-border payments might be simplified greatly.

Everything remains the same for now, though, and understanding the IBAN vs SWIFT purpose will very much continue to shape the relations of people involved in dealing with money at an international level.

Conclusion:

Final Thoughts: Understanding the SWIFT code vs IBAN differences is not just grasping banking keywords – it is claiming authority over your international remittances. Whether you’re supporting relatives living in different countries, paying for foreign education, or handling business payments, you will know how and when to use these codes. With international money transfer services available at the tip of your finger, these vitally important codes will save your recipients and you some money while ensuring a more efficient payment system.

Frequently Asked Questions

What is the main difference between IBAN and SWIFT?

SWIFT codes can identify banks, while IBANs recognize a person’s entire bank account. To use easier terms, IBAN is your full address, while SWIFT is the company bringing the mail to your vicinity. SWIFT does not possess any account information except which bank should get the payment should be sent.

Do I need both IBAN and SWIFT to send money internationally?

Where payments are being remitted to is relevant. Within the European area, an IBAN would usually suffice. In comparison, transactions from Europe or certain countries without an IBAN, having both codes, are applicable.

Which one identifies the bank and which one identifies the account?

SWIFT identifies the bank and its location, while IBAN identifies your specific account within that bank. The SWIFT code gets your money to the right institution, and the IBAN makes sure it reaches your exact account number.

Are IBAN and SWIFT codes interchangeable?

No, they’re not interchangeable – they serve completely different purposes. Using one instead of the other would be like trying to use a phone number as a postal address. Each has its specific role in the international transfer process.

Can a transaction go through with only one of them?

Sometimes, but not always. Within the SEPA zone, IBAN alone is usually sufficient. However, for many international transfers, especially to non-IBAN countries, you’ll need both codes. Missing either one can cause delays, extra charges, or failed transfers.

What is the estimated time frame for processing international transfers?

IBAN transfers within SEPA: Same day or next business day. SWIFT wire transfers: 1-5 business days, depending on correspondent bank relationships and the destination country

If incorrect banking codes are provided, what consequences will arise?

Providing wrong codes can lead to significant issues. A wrong IBAN may get rejected/ignored immediately by the sender due to internal validation. However, inaccurate SWIFT codes could pay your money to the wrong bank. Always use confirmation codes before proceeding with transactions.

Are there alternatives that offer better pricing than traditional bank transfers?

Of course! Online services for money transfer like Wise, Remitly, or WorldRemit usually present better prices and lower fees than standard banks. While they operate within the same infrastructure using Bank Identifier Codes (BICs) and SWIFT codes, they choose to pass the savings to their customers.

Leave a comment