Discover the meaning of remittance, how it works, and its role in sending money abroad safely and efficiently.

What Is Remittance: A Comprehensive Guide for International Transfers

In this era of globalization, remittances play a crucial role in supporting families across borders. A remittance is not merely about sending money; it represents love, social duties, and family bonds that help meet basic needs, including education, medical treatment, shelter, and other daily requirements.

This guide covers every aspect of remittances, including definitions and practical advice on sending and receiving money from abroad.

What is a Remittance? Understanding the Basics

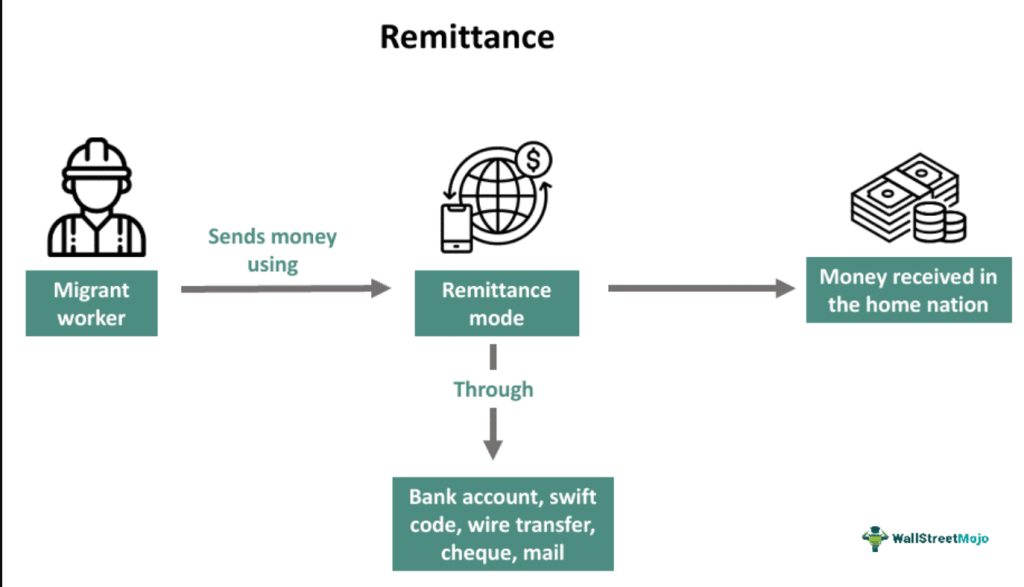

A remittance refers to funds transferred from one person to another across borders via international payments. The term comes from the word “remit,” which means “send back.” While any transaction could be a remittance, the term is most broadly associated with international transfers, primarily those sent by expatriate workers to their relatives in their home country.

Remittances are financial bridges connecting people separated by geographical distances but linked by familial or friendship ties.

Types of Remittances

Remittances can be classified into two broad categories:

1. Personal Remittances

These are payments made between individuals, usually family members, such as in the following scenarios:

- A nurse residing in the US wiring funds to her children located in India

- IT employees from Germany supporting their ageing parents in India

- Migrant workers assisting broader family members who used to live in the country of their migration

a. Person-to-Business (P2B) Remittances

Transfers made by individuals to a business entity or a designated service company offshore. These encompass:

Tuition Fee Payments

- International students remitting tuition fees to their host institutions

- Funds sent by parents to aid their children’s education abroad

- Payment for related costs, which include residence, books, and other academic materials

Healthcare Payments

- Patients remitting for healthcare services not available in their countries of residence

- Medical tourism payments for surgeries, specialized treatments, or consultations

- Insurance reimbursements for services rendered abroad

Travel Remittances

- Remittances sent for travel and holiday expenses

- Emergency aid for persons travelling overseas

- Pre-funding of travel cards/accounts for expected upcoming trips

2. Business remittances

- Payments through businesses across borders, such as an Australian company paying its supplier in Vietnam.

- Real estate purchases or investments

- Investing in foreign companies or startups

- Payment of goods and services rendered by offshore suppliers

- Payment for professional services rendered (legal, consulting, etc.)

Remittances tell a fundamentally human story. Consider Ahmed, a software engineer working in Dubai, who sends $1,200 every semester to cover his daughter’s tuition fees and living expenses as she pursues her engineering degree at a university in Canada. Each month, he also transfers an additional $500 to help with her accommodation, books, and daily expenses. Multiplied by millions of parents globally supporting their children’s education abroad, this simple act forms an enormous economic force that often surpasses official development aid.

Remittances and Their Global Impact

The financial scale of remittances is staggering. According to the World Bank, officially recorded remittances sent to low and middle-income countries reached $626 billion in 2022, over triple the amount of official development assistance and in many cases exceeding foreign direct investment.

1. Economic Impact as Percentage of GDP

Some countries rely heavily on remittances as part of their GDP:

- Tonga: 43.9% of GDP

- Lebanon: 38% of GDP

- El Salvador: 26.2% of GDP

- Nepal: 24.8% of GDP

- Honduras: 23.4% of GDP

2. Largest Remittance Recipients by Volume

- India: $100 billion

- Mexico: $60 billion

- China: $51 billion

- Philippines: $38 billion

- Pakistan: $30 billion

Source: World Economic Forum

“Remittances are a lifeline for developing economies and vulnerable populations, providing a critical buffer against economic shocks and supporting household consumption and investment.” – World Bank Group

3. Social Impacts of Remittances

Beyond economic impacts, remittances have far-reaching social effects:

- Poverty eradication: Directly raising household income above poverty lines

- Educational attainment: Funding tuition and school supplies, allowing children to remain enrolled

- Access to healthcare: Paying for medical care and improving health outcomes

- Improved housing: Funding repairs, renovations, and home purchases

- Entrepreneurship: Stimulating small business creation through local capital infusions

Remarkably, remittances often persist through economic downturns. During crises, migrants frequently send more money home rather than less, contrary to expectations.

How Remittance Systems Work: Following the Money

The basic remittance process follows a similar pattern regardless of method:

- Initiation: The sender (remitter) provides payment details and funds (including fees) to a service provider

- Processing: The service provider processes the transaction, including currency conversion

- Transmission: Transfer instructions are sent through the provider’s network

- Distribution: The recipient receives funds through the designated method (bank deposit, cash pickup, mobile wallet, etc.)

- Confirmation: The sender receives confirmation of successful delivery

Remittance Channels

Bank Transfers

Bank-to-bank transfers often involve the SWIFT network (Society for Worldwide Interbank Financial Telecommunication). While secure, they typically have higher fees and can take several business days to process.

Money Transfer Operators (MTOs)

Companies like Western Union, MoneyGram, and Ria offer cash-to-cash transfers through global networks. MTOs are often faster than banks, sometimes providing transfers in as little as 10 minutes and serving regions with limited banking access.

Online Remittance Services

Digital-native companies like Remitly, WorldRemit, and Fairexpay money transfer services are disrupting the market with lower fees and competitive exchange rates. Funds are typically deposited directly into the recipient’s bank account or mobile wallet.

Mobile Money Services

In areas with limited bank access but available mobile service, mobile money platforms have transformed remittances. Services like M-Pesa (Kenya), GCash (Philippines), and bKash (Bangladesh) enable direct deposits to mobile numbers, which can then be spent, withdrawn as cash, or used for bills.

M-Pesa alone has helped lift approximately 2% of Kenyan households out of extreme poverty, with especially strong effects among women-headed households.

Informal Channels

A significant portion of remittances flows through informal services operating on trust networks without legal financial structures, such as hawala (Middle East/South Asia) or hundi (India). While these may offer lower costs and reach remote areas, they lack consumer protections and pose potential risks.

Inward vs. Outward Remittances

Remittances are classified based on their direction relative to a specific country:

Inward Remittances

Funds are coming into a country from overseas. From the receiving country’s perspective, this represents an inflow of currency.

Example: If you’re in India and your brother working in the UAE sends you money, that’s an inward remittance from India’s perspective.

Characteristics:

- Less stringent documentation requirements

- More favorable foreign exchange rates

- Fewer restrictions on fund usage

- Possible tax exemptions in some jurisdictions

Outward Remittances

Money sent from within a country to a recipient abroad represents a currency outflow from the sending country’s perspective.

Example: If you’re working in the UAE and send money to your parents in India, that’s an outward remittance from the UAE’s perspective – money flowing out of the UAE to another country.

Characteristics:

- Stricter documentation requirements

- Regulatory limits on transaction amounts

- Purpose declarations required

- Potential tax implications or reporting obligations

Countries tend to be more restrictive with outward remittances, especially those with currency controls or fixed exchange rates. For instance, China restricts individuals to $50,000 in outward remittances annually, while India permits up to $250,000 per financial year under its Liberalized Remittance Scheme.

How to Send a Remittance: Step-by-Step Guide

1. Research Your Options

Evaluate service providers based on:

- Overall price including exchange rate markup

- Transfer speed

- Delivery method accessibility at the destination

- Coverage in the recipient’s location

- Reliability and reputation

- User satisfaction with digital options

Comparison sites like Monito and Finder can help find suitable options.

2. Compile Essential Information

You’ll typically need:

- Recipient’s full legal name

- Destination country and currency

- For bank deposits: Bank name, account number, branch information, routing codes (SWIFT/BIC, IBAN)

- For cash pickup: Recipient’s phone number and address

- For mobile money: Recipient’s mobile wallet number

3. Prepare Relevant Documentation

Depending on the amount and destination, you may need:

- Identification document (Aadhar, PAN card, passport, driver’s license)

- Source of funds documentation for large amounts

- Remittance application form

4. Complete the Transfer Request

Following the service provider’s procedures:

- Enter recipient information

- Specify the amount to send

- Review the exchange rate and fees

- Provide payment method (bank account, card, cash)

- Complete any verification requirements

5. Monitor the Transfer

Most providers offer tracking options:

- Reference or tracking number

- Status checks via app or website

- SMS or email notifications

- Customer service contact for issues

6. Inform the Recipient

Let them know:

- Payment is being processed.

- Expected arrival time

- Any reference numbers needed

- Collection requirements (identification, etc.)

7. Verify Receipt

Ensure the payment was received and the amount matches exactly. If problems occur, immediately contact your service provider with tracking details.

Remittances and Financial Inclusion

Remittances foster financial inclusion by enabling the productive use of technology in underbanked communities:

- Savings accounts: Recipients are motivated to save portions of the received funds

- Credit history development: Regular remittances help establish financial records supporting loan applications

- Insurance products: Some providers bundle remittance services with life, health, or property insurance

- Investment opportunities: Remittances provide capital for education, micro-investments, or future funding

Countries with significant remittance inflows tend to experience corresponding increases in bank account ownership and formal savings. In India, adult bank account ownership rose from 53% to 78% between 2014 and 2021.

Common Issues and Solutions

Transfer Delays

Problem: Delayed arrival.

Solutions:

- Choose faster (though more expensive) options

- Avoid initiating transfers during weekends or holidays

- Provide complete recipient details

- Use tracking systems to monitor progress

High Costs

Problem: Excessive fees and unfavorable exchange rates.

Solutions:

- Compare multiple providers, including exchange rate markups

- Consolidate smaller transfers into larger ones

- Look for promotional offers

- Consider Fairex remitted with lower pricing

Transfer Rejections

Problem: Transactions are getting rejected.

Solutions:

- Double-check all details for accuracy

- Verify that the recipient account can accept foreign transfers

- Ensure purpose codes or declarations are correctly completed

- Document all attempts and communications

Exchange Rate Fluctuations

Problem: Rate changes between initiation and receipt reduce transfer value.

Solutions:

- Use providers offering guaranteed rates

- Monitor exchange rates and transfer during favorable periods

- Consider multiple smaller transfers to average out rate fluctuations

Fraud and Scams

Problem: Fraudulent activities targeting senders and recipients.

Solutions:

- Use only licensed and regulated service providers

- Share transfer codes only with intended recipients

- Verify unexpected transfer requests

- Confirm changes to recipient information through secure channels

When issues arise, document everything and contact the service provider immediately.

Conclusion: Remittances as Financial Bridges

Remittances represent more than just money transfers; they embody love, bonds, and responsibility. They fund education, healthcare, housing, and dreams worldwide, providing stability during crises and investing in prospects.

The remittance industry continues to evolve rapidly, driven by new technologies, competition, and changing migration patterns. These trends promise increasingly faster, cheaper, and easier cross-border transfers, whether through digital wallets or traditional bank-to-bank money transfer methods, unlocking greater economic and social benefits.

Whether you’re a migrant worker supporting family back home, a parent paying for overseas education, or someone helping a friend in another country, understanding remittances empowers you to make smart decisions about international money movement.

By participating in remittances, you’re engaging in one of the most important forms of global financial exchange, one that connects people, supports lives, and maintains relationships across borders.

FAQ

What differentiates a remittance from a bank transfer?

While all remittances involve transferring money, not all money transfers are remittances. The term “remittance” typically refers to transfers between individuals across national borders, often for family support. Bank transfers are one method of sending remittances, alongside money transfer operators, post offices, mobile money, and informal networks.

Are remittances subject to taxation?

Restrictions apply to outward remittances from India, which fall under Tax Collection at Source (TCS), owing to the Liberalised Remittance Scheme (LRS). For remittances over ₹7 lakh in a financial year, a 5% TCS is mandatory (increased for some categories, including foreign tour packages). Conversely, personal remittances sent to individuals in India, like funds sent by relatives from overseas, are exempt from taxes for the recipient except under special circumstances where they may be deemed as taxable income (for instance, salary or fees). Taxes are complicated as they can change due to purpose and amount, which requires the consultation of a tax expert or reviewing the most recent government publications.

How long does it take to receive a remittance?

Processing times vary from minutes to days, depending on:

- Service provider

- Destination country

- Payment and delivery methods

- Verification processes

- Banking hours and holidays

Digital transfers to bank accounts typically take 1-3 business days. Cash pickup options may be available within minutes, and mobile money transfers process almost instantly.

What happens if the recipient details are incorrect?

If the error is caught during processing, the transfer may be cancelled and returned minus a fee. If only part of the information is wrong (like a misspelled name), the recipient may have trouble collecting the funds. If an account number is invalid but plausible, the money might get stuck until it is resolved through lengthy procedures. Always triple-check recipient information before finalizing transfers.

Can I cancel a remittance after sending it?

This varies by case:

- Some providers allow cancellation if funds haven’t been claimed

- Cancellation fees may apply during processing

- Completed transfers generally cannot be cancelled

Contact your service provider immediately to maximize cancellation chances.

Are there restrictions on remittance amounts?

Yes, at multiple levels:

- Service providers impose transaction limits (cash pickup services typically have lower limits)

- Sending countries may restrict outward remittances (especially those with currency controls)

- Receiving countries may impose limits or require additional documentation above certain thresholds

- Large transfers trigger legal reporting requirements

Restrictions vary significantly by country and provider.

What identification is required to send a remittance?

Most transfers require a government-issued photo ID, such as a passport, driver’s license, or national ID card. Some providers also require proof of address, source of funds documentation (for larger amounts), and information about the transfer’s purpose. Cash transactions typically face stricter requirements than digital transfers from bank accounts.

Leave a comment