Step-by-step guide to sending money from India to other countries, covering methods, charges, and required documentation.

How to Send Money Abroad from India: Your Complete Step-by-Step Guide for International Money Transfers

Last month, I remember Priya, my friend from college, was trying to figure out a way to pay her son’s university fees in Canada. Priya used to go to a bank and wire transfer the money out there for years. She was losing out on thousands of rupees because of the bank’s exchange rates. Does this sound familiar?

In this guide, I aim to cover everything from Reserve Bank of India policies to the regulations that need to be complied with. This one-stop guide is perfect for anyone looking to transfer money internationally from India for education, support of family, business transactions, etc.

Understanding International Money Transfers: All You Need to Know

With everything under the Reserve Bank of India’s eye, India doesn’t make it easy when it comes to money transfers to foreign companies. Understanding these rules could mean a big difference between an unnecessary regulatory headache and a smooth transfer.

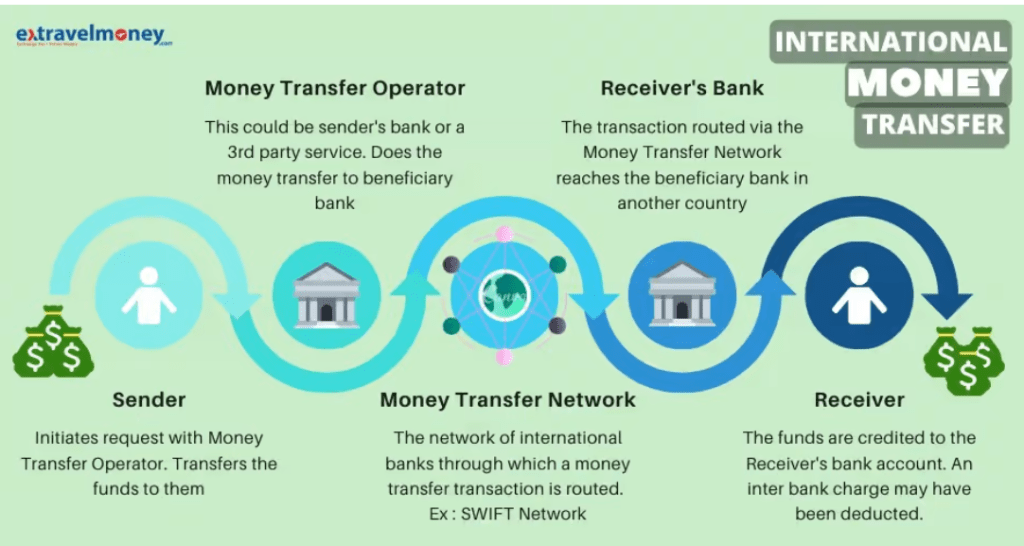

International money transfers from India include payments to overseas accounts, foreign companies, or individuals residing abroad. This covers:

- Payment of the family

- Business-related payments

- Insurance premiums of overseas countries

- Travel expenses

- Tuition fees (within USD 10K)

Under the Liberalized Remittance Scheme (LRS), the Indian government permits its residents to transfer a specific amount of money abroad. Consider LRS as your yearly limit set for overseas transactions – currently pegged at $250,000 per financial year on a per capita basis. This cap is inclusive of everything, including education and purchasing of foreign properties, thus making it critical to map out your transfers strategically.

Primary Factors for International Remittances

As per the data from the RBI, Indians remit through legal means more than $18 billion every year. Notably, the main reasons are:

- Education expenditure (40% of total remittance)

- Family maintenance and support (25%)

- Medical treatment overseas (15%)

- Travel and tourism (12%)

- Business-related activities (8%)

Having a clear rationale for the transfer helps in choosing the most suitable method and form of documentation needed.

Legal Framework: RBI’s Guidelines on Outward Remittance

The RBI guidelines for outward remittance form the foundation of the country’s foreign exchange regulatory framework in the country. These are not regulations for the sake of bureaucracy. They serve the purpose of providing certain equilibrium for the economy of the country while facilitating genuine cross-border interactions.

In the existing structure, any resident Indian can remit up to $250,000 in a single calendar year without requiring additional approvals. Nonetheless, this flexibility comes with certain limitations:

Transactions Permitted Include:

- Visiting friends and relatives abroad

- Remittance, either as a gift or a donation

- Emigration

- Seeking medical treatment

- Pursuing education abroad

- Maintenance of close relatives

Transactions Not Permitted Include:

- Sponsoring contests or raffles

- Gambling or any form of wagering

- Foreign exchange dealings outside the country

- Investment in companies engaged in the real estate business

The beauty of understanding these guidelines is how simple they are. Familiarity with the existing framework allows for seamless remittance. Too many have underestimated the rules and, as a consequence, have overthought legitimate remittances.

Required Documents According to RBI Guidelines

Documentation is essential for every international money transfer. Documents for outward remittance differ according to the amount of money transferred and the purpose behind it:

For Payments Less Than ₹25,000:

- Purpose self-declaration

- Current PAN card

- Bank account information

For Amounts Exceeding ₹25,000:

- Form A2 (declaration cum application)

- CA certificate for amounts exceeding $50,000

- Additional documents supporting the claimed purpose

- Passport with Visa (if applicable)

Step-by-Step Guide: How to Send Money Abroad from India

I will present the entire process in simple steps. Based on my experience helping friends and family with international transfers, I can attest that being prepared alleviates the burden significantly.

Step 1: Determine Your Transfer Amount and Purpose

Before opting for any service, make sure to assess the amount of funds you will be transferring. This goes beyond choosing a principal amount; also, figure out the following:

- Exchange rate volatility (can increase or decrease by 2-5% daily)

- Service charges (₹500 to ₹2,000 for most providers)

- Charges from intermediary banks (between ₹1,000 and ₹3,000 for telegraphic transfers)

- Goods and service tax on transfer fees (18% on service fees)

As an illustration, when you send $10,000 for education, your total expenses will be somewhere between ₹8,50,000 to ₹8,80,000 based on your selection.

Step 2: Choose Your Transfer Method

Each option impacts an individual’s costs, speed, and convenience. Allow me to elaborate on what I’ve found for each option:

Traditional Bank Wire Transfers

While banks provide safety and an established method, they are costly. My bank charges ₹1,500 as a flat fee plus 0.25% of the amount being transferred. Exchange rates are 2-3% above the mid-market rate at best.

Online Money Transfer Services

Wise, BookMyForex, and Fairexpay are examples of online money transfer services that have changed how we send money from India abroad. These services have:

- Better exchange rates

- Lower fees

- Transparent pricing

With a switch from traditional services to online services, I’ve personally saved over ₹15,000 each year.

Forex Cards vs Wire Transfers

The forex card vs wire transfer debate usually leaves people perplexed. While forex cards are optimal for travel-related purchases, wire transfers are suited for large, one-off payments like tuition fees or property purchases.

Step 3: Compare Costs and Services

Do not make a choice solely based on the advertised exchange rates. For an accurate assessment, utilize the following calculation:

Total Cost = (Amount × Exchange Rate) + Transfer Fees + GST + Intermediary Charges

Below is a simplified approach that I devised:

- Get the mid-market rate from Google or XE.com

- Identify the markup from each service offered

- The sum total of all costs and charges

- Evaluate the overall final amount disbursed

Money Transfer Methods: Detailed Comparison

| Transfer Method | Processing Time | Typical Fees | Exchange Rate Markup | Best For |

|---|---|---|---|---|

| Bank Wire Transfer | 2-5 business days | ₹1,500-3,000 | 2-4% above mid-market | Large amounts, long-standing relationships |

| Online Services | 1-3 business days | ₹300-1,200 | 0.5-2% above mid-market | Regular transfers, cost-conscious customers |

| Forex Companies | 1-4 business days | ₹500-2,000 | 1-3% above mid-market | High value transactions, tailored service |

| Digital Platforms | Minutes to 24 hours | ₹100-800 | 1-2.5% above mid-market | Fast access, smaller sums |

NRI Money Transfer Options: Special Considerations

There is a stark contrast between NRI money transfer options and those for residents. For NRIs, they can:

- Transfer any amount without restriction from NRE accounts

- Utilize NRO accounts for restricted transfers (up to $1 million per year)

- Benefit from a simplified documentation process

- Access specialized NRI banking services

It’s a common misconception that NRIs have less flexibility than residents, when in fact, they are granted more flexibility for international transfers. This benefit may prove useful for decreasing spending during large-scale transactions.

Cost Optimization: Securing Low-Cost International Transfers

Achieving low-cost international transfers in India is not a simple process; rather, it is a clever strategy. Here’s what I have learned over the years while optimizing my international transfers:

Transfer Timing Strategy

The currency exchange rates are highly volatile and fluctuate at all times. I conveniently track the rates for USD-INR on tools like XE Currency and CurrencyFair. During the strengthening phase for the rupee, I execute planned transfers. During the weakening phase for the rupee, I delay non-urgent payments.

Pro tip: Do not attempt to transfer funds on Fridays or before long weekends, as these periods can attract weekend premiums, which add roughly 0.5-1% to your costs

Understanding Tax Implications

The tax on international transfers has undergone significant evolution over the years. Under the current framework, we operate with the following taxes:

- TCS (Tax Collected at Source): 5% on the amount surpassing ₹7 lakh in a financial year under LRS

- GST: 18% on the service fee for transferring money

- Income tax: Based on the purpose of the transfer

For education, you can claim TCS as an advance tax, which is thus refundable. For other purposes, proper documentation aids tax optimization.

Choosing Speed vs Economy

While sending medical aid to my uncle in the US, I didn’t care much about the cost. However, I was willing to optimize my cost when it came to my daughter’s semester fees.

Fastest Ways to Send Money from India:

- Digital wallets for certain corridors (2-4 hours)

- Online transfer systems such as Wise (major currencies transfer within a day)

- Express wire transfer (24-48 hours)

Most Economical Options:

- Scheduled transfers booked in advance (saves 1-2%)

- Bulk transfers for multiple payments

- Forward contracts (rate locks on future transfers)

Specific Transfer Scenarios and Best Practices

Sending Money for Education

Tuition fees account for the majority of remittances sent from India. In helping many families with this, I learned several important methods.

Paying directly to the university is sometimes better than sending money to student accounts. A good number of universities will accept wires in INR and convert at more favorable institutional rates.

Documents Required for Educational Fund Transfers:

- University offer letter

- Document detailing fee categories and payment timelines

- Student visa (where applicable)

- Form A2 with CA authorization for amounts beyond $50,000

Family Maintenance and Support

Long-term automated support arranged via relationship banking frameworks streamlines regular family support payments. I automated monthly transfers for my parents’ maintenance expenditures in Canada, optimizing:

- Standing transfer instructions, which provide enhanced value for repetitive transactions

- Documented family member identification simplifies future transfers

- Loyalty program benefits are granted after certain thresholds are met

Business and Investment Transfers

Corporate financial transactions require strict compliance protocols; however, they present particular beneficial aspects:

- Increased transfer limits for authentic corporate purposes

- Dedicated corporate banking facilities with lower fees

- Multi-currency capabilities for international business activities

Technology Solutions: Online Money Transfer to Bank Account

International remittance systems have been revolutionized by the ability to send money directly to bank accounts online. Convenience and lower costs are the main drivers behind the trend where more than 60% of outward remittances from India are processed electronically.

Mobile Applications and Online Platforms

Traditional banks are unable to compete with modern transfer apps because they offer:

- Real-time rate alerts (get notified when rates hit your target)

- Transfer tracking (know exactly where your money is)

- Multi-beneficiary management (managing multiple accounts safely)

- Rate guarantees (locking rates for up to 72 hours)

Through rate alerts, I optimize timing for transfers and often save 1-2% by waiting for favorable market movements.

Security and Safety Measures

While digital transfers are often considered risky, licensed platforms often provide better security compared to traditional methods:

Look for These Security Features:

- Two-factor authentication

- Bank-level encryption

- Regulatory compliance (RBI authorized)

- Insurance coverage for failed transfers

Common Mistakes to Avoid

My own experience, coupled with my aid to others, has revealed habits that are loss-oriented:

Documentation Errors

Incorrect or incomplete documentation causes over 30% of transfer delays. Remember:

- Beneficiary name spelling (must match bank records exactly)

- Account numbers and routing codes accuracy

- Purpose codes (incorrect codes trigger compliance reviews)

Timing Mistakes

- Weekend transfers often carry extra charges

- The holiday season triggers higher demand and costs

- Last-minute transfers eliminate rate comparison opportunities

Service Selection Errors

Choosing solely based on advertised rates disregards total costs. Always calculate the final amount your recipient receives to avoid expensive surprises.

Conclusion

Transferring money from India doesn’t have to be costly or complicated. Strategic timing of your payments, selection of the appropriate service provider, and compliance with RBI guidelines can make this process significantly more cost-effective. You might save thousands of rupees annually with the right approach.

While a specific transfer method may work perfectly for your friend, it may not be optimal for your situation. Consider your specific circumstances, transfer frequency, acceptable risk levels, and various other factors when making decisions. Don’t hesitate to experiment with different service providers, as most offer first-time user discounts to test their services.

Frequently Asked Questions

What is the best way to send money abroad from India?

The best possible way varies between individuals. If you need regular transfers below $5,000, online money transfer services like Wise or BookMyForex would be efficient. For bigger amounts, specialized forex companies usually provide the best rates and personalized service. Traditional bank wire transfers work best when you have established relationships, despite expensive fees.

What documents are necessary for international transfers?

Document requirements differ based on the amount being transferred:

- Less than ₹25,000: Self-declaration form along with PAN card

- ₹25,000 to ₹50,000: Form A2 along with purpose documentation, PAN card

- Greater than ₹50,000: All documents mentioned previously plus CA certificate

- Exceeding $250,000: Requires RBI approval

Always have your passport for identity verification and purpose documents (like university admission letters for education transfers).

Are there limits on how much I can send abroad?

Yes, under LRS for sending money abroad, residents are limited to $250,000 per financial year without special approval. This is a per-person limit, so married couples effectively have a cap of $500,000 annually. NRIs have more flexibility: unlimited from NRE accounts and up to $1 million per year from NRO accounts.

How long does it take to send money internationally from India?

Transfer times vary by method:

- Digital platforms: 1-24 hours for major currencies

- Bank wire transfers: 2-5 business days

- Forex companies: 1-4 business days

- Express services: Same day to 48 hours (with premium fees)

Transfers to developed countries (US, UK, Canada) process faster than developing countries due to superior banking infrastructure.

What is the tax on sending money abroad from India?

The existing taxation framework consists of:

- TCS: 5% on LRS transfers above ₹7 lakhs annually (20% if PAN not provided)

- GST: 18% on service charges

- Income tax: Applicable depending on transfer purpose and income bracket

TCS on education and medical expenses qualifies as advance tax, hence it is refundable during tax filing.

Can I cancel an international transfer once initiated?

Cancellation policies differ by provider and transfer stage. Most services allow cancellation within 30 minutes to 2 hours after initiation. After processing begins, cancellation incurs fees (usually ₹500-2,000). Always check cancellation policies before confirming transfers.

Is it better to use a forex card or a wire transfer for international payments?

Forex cards are best suited for:

- Travel expenses and daily expenditures

- Multiple, smaller transactions

- Countries with good card acceptance

Wire transfers are best suited for:

- Large one-time payments (tuition fees, property purchases)

- Direct bank-to-bank transfers

- Countries with limited card infrastructure

How can I track my international money transfer?

Modern transfer services offer multiple tracking options:

- SMS notifications at each transfer stage

- Email updates with reference numbers

- Mobile app tracking with real-time status updates

- Customer service hotlines for instant updates

Preserving your transfer reference number is essential for tracking and customer service inquiries.

Leave a comment