Discover what a Guaranteed Investment Certificate (GIC) is, how it works, and why it’s a safe investment option.

What Is a GIC? Guaranteed Investment Certificate explained: Your 2025 Complete Guide on Investment Certificates.

In this scenario, suppose you have $10,000 saved in a savings account earning an astonishing 0.5 percent interest per annum. The rate is so low that it does nothing to outrun inflation, let alone grow your savings. Does this ring a bell? Right, it does for most people. Luckily, there is an effective way to Secure Investment Certificates that utilize money lost in value due to inflation. GICs are one of the safest investment options in Canada, and earn decent rates of return, making them an attractive option.

GIC is very simple and complicated at the same time; here’s a full guide breaking down everything you need to know from comparison of top providers, understanding what Guaranteed Investment Certificates are, GIC withdrawal rules, along other important decisions around GICs.

Knowing the bank acronyms can be quite overwhelming, and so GICs need a thorough explanation because the Bank also considers GTD (Guaranteed Time Deposit) to be synonymous, and thus will treat both interchangeably.

What Is a Guaranteed Investment Certificate (GIC)?

A Guaranteed Investment Certificate (GIC) is essentially a loan you give to a financial institution in exchange for guaranteed interest payments. Consider it a formal IOU where your bank pledges to return your base principal in addition to some specified interest after a set period.

In essence, the process works as follows: you place a deposit with a bank, a credit union, or a trust company for a specific period known as the GIC maturity period. During this time, the deposit continues to earn interest at either a fixed or variable rate. Upon the expiration of the term, the initial capital, along with all earned interest, is paid back.

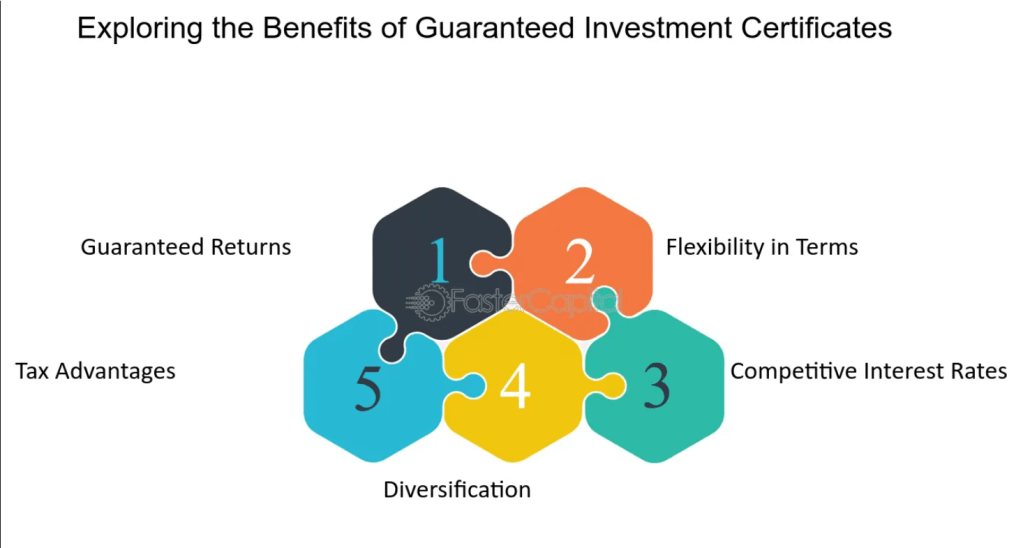

Key Benefits of GICs

Benefits that make GICs attractive include:

- Principal protection: The original investment is guaranteed 100 percent

- Predictable returns: Exact profit figures can be derived

- CDIC insurance: Protecting funds up to $100,000 per institution

- No management fees: Unlike mutual or exchange-traded funds

- Flexible terms: Spanning from 30 days to 10 years

Embracing greater simplicity makes GICs more appealing relative to other forms of securities. Their resilience towards market fluctuations is attractive – if a stock market crash occurs or bond defaults, your GIC will remain unaffected, providing the original capital along with interest. This makes them particularly helpful for conservative investors who prefer lower, but guaranteed yields.

Types of GICs

Fixed-Rate GICs

Standard fixed-rate GICs are the most traditional and easiest to understand. They are akin to a simple flavor of ice cream – classic yet dependable. Fixed-rate GICs allow locking in interest for the whole term, ensuring that you will make money regardless of wider economic conditions.

As of now, the fixed-rate GIC interest rates sit between 2.5% and 4.8%, varying by the institution and term length. As a general rule, longer terms provide greater rewards in the form of higher interest rates.

Cashable vs Non-Redeemable GICs

The withdrawal policies for GICs become increasingly important at this juncture. Cashable GICs allow one to withdraw their funds before the agreed-upon time, although doing so will come at a cost of lost interest. Non-redeemable GICs provide higher interest rates, but in exchange, the funds are permanently locked away.

Comparison of Cashable vs Non-Redeemable GICs

| Feature | Cashable GIC | Non-Redeemable GIC |

|---|---|---|

| Interest Rate | 2.0-3.5% | 3.0-4.8% |

| Early Access | Yes (usually after 30-90 days) | No |

| Rate Guarantee | Lower guaranteed rate | Higher guaranteed rate |

| Best For | Emergency funds | Long-term savings |

Market-Linked GICs

If you’re looking for guaranteed principal protection but expect higher returns, market-linked GICs can be a suitable option as they offer stock-market-linked returns. While your principal is safeguarded, the interest earned is contingent on the performance of certain market indices.

How To Open A GIC Account – Step By Step

The procedure to open a GIC account is simple, but understanding the right way to open a GIC account can help save time while unlocking better rates at the same time.

Step 1: Research and Compare Rates

Look for the best deals from GIC providers in Canada. Big banks like RBC, TD, and Scotiabank have good deals, but better returns are often offered by credit unions and transfer money online.

Step 2: Gather Required Documents

You will need the following:

- Government-issued photo identification document

- Social Insurance Number

- Proof of address

- Funds for an initial deposit of $500 to $1,000, depending on the institution

Step 3: Choose Your GIC Features

Consider:

- Term length: Match with your financial goals

- Minimum deposit: $500 – $1,000, depending on the institution

- Renewal options: Automatic renewal vs. manual decision

Step 4: Fund Your Account

Most organizations let you transfer funds from your bank account. Be cautious of the potential charges for transferring between banks.

(Tip: Review the money transfer charges list from your bank or provider to avoid unexpected fees and ensure the full amount reaches your GIC.)

GIC vs Fixed Deposit – Clarifying the Differences

Newcomers to Canada often ask about the differences between GICs and fixed deposits, especially if they are used to fixed deposits in other countries. While both these investments are considered low risk, there are some subtle differences:

GICs in Canada:

- Have government and provincial regulations

- CDIC insurance protection

- Term option flexibility

- Higher minimum investment requirements in most cases

Fixed Deposits (International Context):

- Same idea, but different regulatory environment

- Insurance for deposits may differ by region

- Tax regulations may vary

- Shorter minimum timeframes in many cases

Top GIC Providers – Where to Get the Best Rates

When choosing from the top GIC providers, you should look beyond the interest rates. Reliability, customer service, and competitive terms are equally important.

Leading GIC Providers in Canada:

- Tangerine Bank: Competitive online rates and an easy-to-use platform

- Meridian Credit Union: Member-centric, frequently offers the highest rates

- Oaken Financial: Offers consistently competitive rates

- Canadian Western Bank: Strong GIC options

- Major Banks (RBC, TD, BMO): Convenient GIC options but often lower rates

Pro Tip: Don’t choose based on your current bank. Online and credit union institutions tend to offer 0.5-1% more than traditional banks.

Special Programs

Student GIC Program

Student GIC programs serve as educational funds and act as a requirement when applying for an international study visa. This particular GIC helps international students earn interest on the funds needed.

Key features of student GICs:

- Minimum $10,000 investment

- Funds are released gradually during studies

- Acceptable for visa applications

- Competitive interest rates

GIC Benefits for NRIs (Non-Resident Indians)

GICs for NRIs come with perks and benefits such as lower taxation and access to foreign currencies. These investments contain withholding taxation for NRIs that should be structured for maximum tax advantages; therefore, professional tax advice is recommended.

Tax Implications – What You Need to Know

GIC interest generates income and is taxed at your marginal rate. However, strategic placement can help counterbalance the overall tax liability:

Tax-Efficient GIC Strategies:

- Hold GICs in TFSAs for tax-free growth

- Use RRSPs for tax-deferred growth

- Consider income splitting opportunities with your spouse

- Time GIC maturities for optimal tax years

Annual tax reporting: A T5 slip showing the amount of interest earned is issued annually, regardless of whether the funds were received (for GICs paying interest at maturity).

Common Errors to Avoid

Having assisted numerous clients with their GIC investments, I have come across these errors time and time again:

- Investing all funds into a single long-term GIC. This precludes you from taking advantage of higher rates should they become available. Consider GIC laddering, where you spread the investments over multiple maturity dates.

- Ignoring inflation erosion. A GIC paying 3% sounds attractive until one realizes that inflation is at 3.5%. Always look at the inflation-adjusted value of returns.

- Not understanding withdrawal terms. Some “cashable” GICs have restrictions or penalties that are not obvious. Always know the fine print.

- Choosing convenience over returns. Banking where it’s easy might result in lost of interest of hundreds of dollars every year.

GIC Laddering Strategy – Optimizing GIC Investments

GIC laddering is the purchase of several GICs with staggered maturity dates. This ensures access to funds regularly while also earning good interest rates.

Example of a 5-Year GIC Ladder:

| Year | Investment | Term | Interest Rate |

|---|---|---|---|

| Year 1 | $10,000 | 1-year GIC | 3.0% |

| Year 2 | $10,000 | 2-year GIC | 3.5% |

| Year 3 | $10,000 | 3-year GIC | 4.0% |

| Year 4 | $10,000 | 4-year GIC | 4.2% |

| Year 5 | $10,000 | 5-year GIC | 4.5% |

After the maturity of the first GIC, renew into a fresh 5-year term. This approach maintains liquidity while capturing better long-term rates.

Conclusion – Is a GIC Right for Your Financial Goals?

Guaranteed Investment Certificates may not be the most exhilarating investments, but they fulfill crucial functions in diversified portfolios. They are ideal for your emergency funds, short-term savings objectives, or the conservative parts of your retirement planning.

Always assess your risk appetite, investment timeframe, and overall financial strategy before investing. GICs are most effective when you know what you will receive in return: absolute safety and reliable returns, albeit lower than stocks or other growth-oriented investments.

Remember, good investing practice is not about trying to identify the one perfect investment – it’s about creating a strategy that allows you to work towards your financial goals with minimal stress, providing peace of mind. Many Canadians find that GICs offer a balanced combination of safety and reasonable returns.

Would you like to explore other GICs? You may wish to start by assessing rates from various providers. It may also be helpful to consult a specialist to analyze the role of GICs in your overall investment strategy.

Frequently Asked Questions About GICs

What is a GIC?

You make a GIC through a deposit with a financial institution for a predetermined length of time. During this term, the financial institution pays you guaranteed interest for the use of your money. At the end, you get the money you deposited and the agreed interest on top.

Who should invest in a GIC?

A GIC would be suitable for conservative investors, elderly investors, people who are in the process of starting an emergency fund, or anyone who values the preservation of their funds over growth. It is also ideal for those investors who wish to avoid the stress of market fluctuations.

What is the risk profile of GICs?

The primary risks are:

- Inflation risk: Gaining a return that doesn’t match rising economic costs

- Interest rate risk: Missing out on higher rates if they rise post-investment

- Liquidity risk: Funds are unable to be accessed for the entire term duration

- Opportunity cost: Potential earnings lost due to funds not being available for other investments

Can I withdraw funds from a GIC before the term expires?

This depends on the type of GIC. For cashable GICs, early withdrawal is permitted but comes with penalties. For non-redeemable GICs, no early withdrawal is allowed except in extreme cases, like terminal illness, and even then, heavy penalties apply.

What happens in the event of a bank failure?

CDIC (Canada Deposit Insurance Corporation) protects your GIC up to $100,000 per institution. This means if your bank fails, you’re guaranteed a refund on the amount within the insured limit.

Are GIC earnings taxable?

Yes, GIC interest is considered taxable income. You will incur taxes at your marginal tax rate on interest income, regardless of whether it is paid out yearly or at maturity. However, GICs within a Tax-Free Savings Account (TFSA) grow tax-free, and those held in a Registered Retirement Savings Plan (RRSP) grow tax-deferred.

What’s the minimum amount needed to buy a GIC?

Most financial institutions have a minimum initial investment requirement between $500 to $1,000. Some may accept as low as $100. Increased funding often comes with better investment rates.

Should I choose fixed or variable rate GICs?

If interest rates are likely to fall or remain stable, fixed-rate GICs provide certainty and are more advantageous. Variable-rate GICs are beneficial in rising-rate environments, but add uncertainty about the total returns at maturity.

Leave a comment