Learn what an IBAN is, how it’s used in international banking, and why it’s important for secure and accurate global money transfers.

What Is an IBAN? Complete Guide to International Bank Account Numbers

Are you planning to send or receive money from abroad? If yes, then IBAN (International Bank Account Number) is something you must understand. International wire transfers can seem complex at first, but this comprehensive guide will help you navigate everything about IBAN and international banking without confusion.

IBAN definition: What is IBAN and Why Is It Important?

IBAN number meaning: IBAN stands for International Bank Account Number. It provides a uniform and standardized method of identifying bank accounts across borders, acting like a ‘lingua franca’ for all banks worldwide.

Why IBAN: Before IBAN existed, international banking was complicated because each country had its own account format, which caused delays and transfers to get stuck. The IBAN system was established in 1997 by the ISO (International Organization for Standardization) with legislation number 13616. Initially intended to facilitate euro payments within European Union member countries, it’s now adopted by more than 70 countries.

Key Benefits of IBAN

- Reduces errors in international transfers

- Streamlines processing speed for cross-border payments

- Ensures funds reach their intended destination without unnecessary delays

- Enables automated routing of payment systems through standardization

“The introduction of the International Bank Account has been one of the most significant improvements in international banking in recent decades. It has reduced error rates for cross-border transactions by over 70%.” European Payments Council

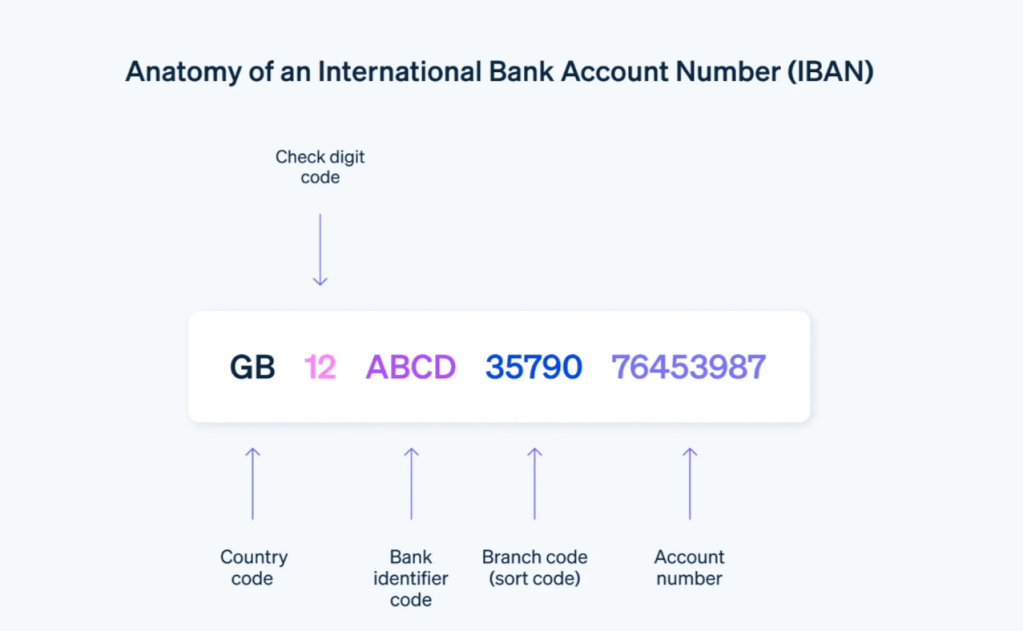

Understanding IBAN Structure Explained

How IBAN works: While an IBAN may appear to be random letters and numbers, each segment contains specific information for smooth payment processing:

IBAN code components: Components of an IBAN

- Country Code: First two letters indicating the account’s country (e.g., GB for the United Kingdom, DE for Germany)

- Check Digits: The Next two numbers for validation and error detection

- Bank Identifier Code: Identifies the specific bank

- Branch Code: Identifies the specific branch of the bank

- Account Number: The individual account number within that branch

IBAN Length and Format by Country

| Country | IBAN Length | Structure | Example |

|---|---|---|---|

| France | 27 characters | FR + 25 characters | FR14 2004 1010 0505 0001 3M02 606 |

| Germany | 22 characters | DE + 20 characters | DE89 3704 0044 0532 0130 00 |

| Italy | 27 characters | IT + 25 characters | IT60 X054 2811 1010 0000 0123 456 |

| Spain | 24 characters | ES + 22 characters | ES91 2100 0418 4502 0005 1332 |

| Netherlands | 18 characters | NL + 16 characters | NL91 ABNA 0417 1643 00 |

| Austria | 20 characters | AT + 18 characters | AT611904300234573201 |

| UK | 22 characters | GB + 20 characters | GB29 NWBK 6016 1331 9268 19 |

IBAN example format: IBANs can have up to 34 characters maximum. Countries often format IBANs with spaces for easier reading, but both “ES9121000418450200051332” and “ES91 2100 0418 4502 0005 1332” are equally valid.

Global IBAN Adoption

1. Countries That Use IBAN

The IBAN system is widely adopted in over 70 countries, concentrated in:

- All EU Member States: Complete adoption across all European Union countries

- EEA Non-EU Members: Including Norway and Iceland

- Middle Eastern Countries: Saudi Arabia, UAE, Kuwait, and others

- Caribbean Nations: Multiple Caribbean countries

- North African Countries: Tunisia and Mauritania

2. Major Economies That Don’t Use IBAN

- United States: Uses ABA routing numbers and account numbers

- Canada: Uses institution numbers, transit numbers, and account numbers

- Australia: Uses BSB (Bank-State-Branch) codes and account numbers

- China: Uses CNAPS codes

- Japan: Uses Zengin codes for domestic transfers

How to Find IBAN?

1. Common Locations for Your IBAN

- Bank Statements: Shown on both printed and electronic bank statements

- Online Banking: Usually displayed on the account homepage or in:

- Account information/details section

- IBAN/International payments section

- Account overview/summary page

- Mobile Banking Apps: Found in the account details sections

- Debit Cards: Some European cards display partial IBAN information (less common due to security concerns)

- Contact Your Bank: Customer service can provide your IBAN via phone or email

- Online IBAN Calculators: Third-party tools that generate IBANs from account details

2. Security Tip

While sharing your IBAN is generally safe for receiving payments, be cautious about who you share it with. In most countries, an IBAN alone cannot be used to withdraw funds from your account.

IBAN Banking System: Common IBAN Problems and Solutions

1. Issues with Incorrect IBANs

- Transfer Rejection: IBAN Banking systems validate IBANs using check digits

- Delayed Processing: Error correction can add days or weeks to transfer times

- Misdirected Payments: Rare cases where funds go to the wrong accounts

- Additional Fees: Failed transfers often result in extra charges

2. How Check Digits Prevent Errors

The two check digits in an IBAN use a sophisticated algorithm to catch common mistakes:

- Transposed digits (12 written as 21)

- Missing digits

- Incorrect characters

3. What to Do If You Use the Wrong IBAN

- Contact your bank immediately to try to stop the transaction

- Provide correct information for future attempts

- Keep all transaction documentation for tracking

- Be prepared for additional time to resolve issues

- Consider sending a small test amount before larger transfers

IBAN Transfer Costs and Fees

1. Standard Charges

- Sending Bank Fee: $15-$50 fixed charge (varies by institution)

- Intermediary Bank Fees: Charged when banks don’t have direct relationships

- Receiving Bank Fee: Up to $30 for processing incoming transfers

- Foreign Exchange Markup: Usually 3-5% above mid-market exchange rates

2. Cost Reduction Strategies

- Use Modern Transfer Services: Wise, Revolut, and similar services often offer better rates

- Compare Services: Fees and exchange rates vary significantly

- Send Larger Amounts: Minimize the impact of flat fees by consolidating transfers

- Choose Optimal Currency: Sometimes better to send in the recipient’s currency

- Check for Fee Waivers: Premium accounts may qualify for discounts

IBAN Security Best Practices

A. What Someone Can Do With Your IBAN

Possible Actions:

- Make payments into your account.

- Access limited information about your bank and country

- Set up direct debits in some territories (varies by country)

What They Cannot Do:

- Withdraw money from your account

- Access online banking

- View account balance or transaction history

- Access confidential information beyond what IBAN reveals

B. Security Recommendations

- Verify Payment Details: Confirm recipient information through multiple channels.

- Use Secure Networks: Avoid public WiFi for banking; use VPNs when necessary.

- Set Up Alerts: Monitor international transactions with notifications

- Regular Account Reviews: Check statements periodically for unauthorized activity

- Avoid Phishing: Never provide banking information via email links

- Set Transaction Limits: Use dedicated accounts with lower limits for international transfers

IBAN vs. Other Banking Codes

1. IBAN vs. SWIFT/BIC Codes

- IBAN: Identifies a specific account (like a complete address)

- SWIFT/BIC: Identifies a specific bank (like the name of a post office)

- Usage: Both codes are often required together for international transfers

2. IBAN vs. US Routing Numbers

- US System: Uses 9-digit ABA routing numbers for domestic transfers

- International: US banks use SWIFT codes for international payments, not IBAN

- Compatibility: US banks can still process IBAN transfers from other countries

Processing Times for IBAN Transfers

| Transfer Type | Processing Time |

|---|---|

| Within the SEPA Zone | 1 Business Day |

| Outside SEPA (Developed Markets) | 2-4 Business Days |

| To/From Developing Markets | 5+ Business Days |

Factors Affecting Speed:

- Banks involved in the transfer

- Currencies being exchanged

- Time of transfer initiation

- Compliance review requirements

Useful IBAN Tools and Resources

Online Validators and Calculators

- IBAN.com: Comprehensive IBAN validation and country information

- SWIFT IBAN Registry: Official registry maintained by SWIFT

- IBAN Calculator: Validates and generates IBANs from national account formats

Conclusion

Understanding IBAN is essential for anyone involved in International money transfers. Whether you’re traveling, conducting international business, or sending money to family overseas, proper IBAN knowledge ensures smoother, more cost-effective transactions.

Key Takeaways

- Always double-check IBAN accuracy before sending funds

- Understand the complete cost structure of international transfers

- Keep records of all international transactions

- Use appropriate tools and services for your specific needs

- Stay informed about security best practices

As international commerce continues to grow, IBAN’s importance as a global banking standard will only increase. With this guide, you’re now equipped to navigate international banking with confidence.

Frequently Asked Questions

- Is it safe to share my IBAN?

Generally, yes, when receiving payments. Unlike credit card numbers, IBANs typically only allow credits to accounts, not debits. However, exercise caution with whom you share this information.

- Why doesn’t the United States use IBAN?

The US banking system was developed separately, with routing numbers and account numbers. As the issuer of the primary reserve currency, the US has less incentive to adopt international standards, though US banks can still process IBAN transfers.

- Can I have multiple IBANs?

Yes, each bank account typically has its own unique IBAN. Many people maintain multi-currency accounts with separate IBANs for different currencies.

- What’s the difference between domestic and international IBANs?

There’s no difference; the same IBAN works for both domestic and international transfers within IBAN-participating countries. The IBAN structure simply contains more detailed information than traditional domestic account numbers.