Exporters lose money after getting paid due to four silent leaks: SWIFT intermediary deductions, FX spread applied at conversion, settlement float cost (days your money sits idle), and reconciliation inefficiency. On a USD 25,000/month business, these combined losses can exceed USD 600–900 per month — or roughly 2.5–3.5% of revenue — without a single line item on your bank statement explaining why.

You Invoiced. You Got Paid. So Why Does Something Feel Off?

Most exporters have been there. The payment shows as received. The USD amount matches the invoice. You tell your team it’s cleared. Then the INR credit hits your account — and the number is slightly lower than you expected. Not dramatically. Just enough to make you check the rate, shrug, and move on.

That shrug is costing you money every single month.

The problem isn’t that export payments are unreliable. The problem is that the gap between what your buyer sends and what you actually receive is built into the infrastructure — invisibly, across multiple points in the chain. And because it never appears as a single line item, most businesses never see it, let alone fix it.

If you’re collecting USD 25,000 or more per month, this is not a rounding error. This is a meaningful portion of your realized revenue that never materializes.

The Four Points Where Exporters Lose Money

1. SWIFT Intermediary Deductions

When your buyer sends a SWIFT wire from their US bank, that transfer doesn’t travel directly to your Indian account. It passes through one, sometimes two, correspondent banks in between. Each of those correspondents may deduct a processing fee — typically USD 15 to USD 45 per transaction.

This depends on whether the transfer was sent as OUR (buyer bears all charges), SHA (charges split), or BEN (you bear all charges). Most buyers default to SHA without thinking about it. Many exporters never check which code is being used.

On ten transactions a month at SHA, you could be absorbing USD 150 to USD 250 in deductions that you never billed for and never agreed to.

2. FX Spread at Conversion

When your USD lands in the banking system, it needs to be converted to INR. The rate applied to your conversion is not the market rate you see on Google or Bloomberg. It is the rate your bank has decided to offer you — which includes a spread above or below the interbank rate.

For SME exporters, this spread typically ranges from 0.5% to 2%, sometimes higher. On USD 25,000, a 1.5% spread means your bank pockets approximately USD 375 per month from this conversion alone.

This is not disclosed as a charge. It does not appear on your statement as a fee. It simply reduces the INR you receive — and because the market rate fluctuates, it is nearly impossible to notice without actively tracking it.

3. Settlement Float Cost

SWIFT payments typically take two to five business days to settle. During that time, your money is sitting somewhere in the correspondent banking chain — not earning returns, not available to your business.

For businesses managing working capital tightly, delayed settlement creates a real cost. If you’re borrowing against receivables or managing vendor payment cycles, every day of settlement delay has a measurable operational cost.

For a business collecting USD 300,000 annually, even a two-day settlement delay across all transactions represents meaningful float cost in working capital terms.

4. Reconciliation Inefficiency

This one doesn’t show up as a financial loss directly — but it compounds the others. When payments arrive without consistent references, or when SWIFT deductions change the amount received versus the amount invoiced, your finance team spends time matching, investigating, and correcting.

That’s staff cost. It’s also delayed reconciliation, which delays tax compliance, FEMA documentation, and BRC filing timelines.

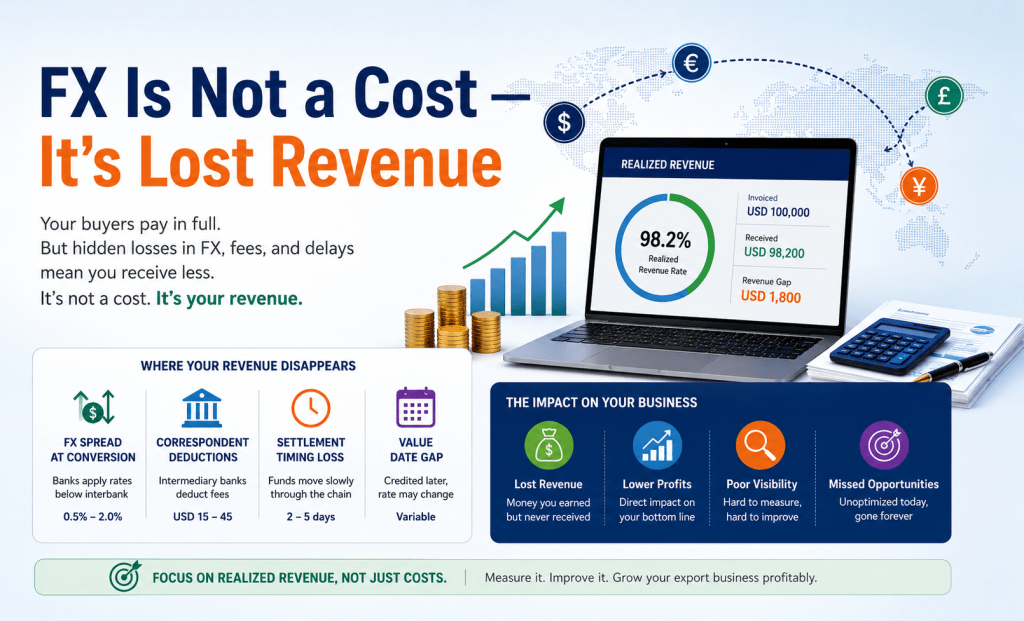

What This Looks Like at USD 25,000 Per Month

| Loss Category | Typical Range | Monthly Impact (USD 25k) | Visibility on Statement |

|---|---|---|---|

| SWIFT intermediary deductions | USD 15–45 per txn | USD 150–300 | Not itemized |

| FX spread at conversion | 0.5%–2.0% | USD 125–500 | Not disclosed |

| Settlement float opportunity cost | 2–5 days per payment | Indirect | Not shown |

| Reconciliation labor cost | Variable | Staff time | Not shown |

| TOTAL ESTIMATED LOSS | ~2%–3.5% of collections | USD 275–800 | Invisible |

At the lower end of this range, that’s USD 3,300 a year you’re not collecting. At the higher end, it’s nearly USD 10,000 annually. And this is for a business at just the USD 25k/month threshold.

Why Finance Teams Rarely Catch This

It’s not because your finance team isn’t doing its job. It’s because the traditional export payment workflow was never designed for this level of visibility.

Your bank statement shows INR received. It does not show INR you should have received. There is no variance report. There is no FX attribution. There is no intermediary deduction log. You would have to manually reconstruct the transaction chain from multiple sources to see the complete picture — and almost nobody does that for every payment.

This is exactly why realized revenue tracking has become a core treasury function for sophisticated exporter businesses. It’s the discipline of measuring not just what came in, but what should have come in.

What You Can Actually Do

The good news is that this problem is solvable — not completely, but substantially.

- Switch to local collection accounts for USD, EUR, GBP, and CAD collections. When your buyer pays locally (like a domestic bank transfer), correspondent banking deductions largely disappear. Your payment arrives clean, with full amounts, faster.

- Benchmark your FX rate on every conversion. Ask your bank for the rate applied and compare it against the interbank rate for that day. The gap is your cost. Tracking it consistently creates accountability and gives you data to negotiate.

- Track realized revenue per transaction, not just total INR received. The question isn’t just ‘how much INR did I get’ but ‘what was the effective USD equivalent I received after all costs.’ This number is your real revenue.

- Choose infrastructure that shows you FX rates before conversion, not after. Transparency at the point of conversion is a structural advantage. If you can see the rate and decide timing, you retain control over a significant revenue variable.

- Consolidate payment references. Ensure every international payment has a consistent invoice reference. It reduces reconciliation cost and makes FEMA documentation significantly cleaner.

The Bigger Picture

International payments are not just an operational function for exporters. They are a revenue function. The difference between what your buyer sends and what reaches your INR account represents the effective monetization rate of your export business.

For businesses at USD 25k to USD 500k per month in collections, even a 1% improvement in that monetization rate is material. It’s the equivalent of finding a hidden revenue stream that required no new sales, no new clients, and no new product.

The businesses that grow their export operations most efficiently are increasingly the ones that treat payment infrastructure as a strategic decision — not just an operational one.

Frequently Asked Questions

Why do exporters lose money even when the buyer pays the full invoice amount?

The full invoice amount rarely reaches the exporter intact. SWIFT intermediary fees are deducted en route, the FX spread at conversion reduces INR received, and settlement delays affect working capital. None of these appear as a single visible charge.

What is FX spread and how does it affect export payments?

FX spread is the difference between the live interbank exchange rate and the rate your bank applies when converting your foreign currency to INR. A 1.5% spread on USD 25,000 means you receive the equivalent of USD 375 less — every single month.

What is the difference between invoice revenue and realized revenue?

Invoice revenue is what you billed your buyer. Realized revenue is what actually reaches your INR account after SWIFT deductions, FX spread, and other costs. The gap between these two numbers is where your money silently disappears.

What are SWIFT intermediary deductions?

When a payment travels via SWIFT, it passes through correspondent banks that each charge a processing fee. These deductions are made from your payment amount, not separately billed. They depend on the charge code (OUR/SHA/BEN) used at the time of transfer.

How can exporters reduce losses on international payments?

The most effective approach is a combination of local collection accounts (to eliminate correspondent deductions), transparent FX pricing infrastructure, and realized revenue tracking at the transaction level. Each reduces a specific leak.

Is there a way to calculate how much I’m losing on international payments?

Yes. For every transaction, compare the INR received against the INR you would have received at the interbank rate that day, with no intermediary deductions. The difference, tracked consistently over a quarter, shows your total payment leakage.

Do local collection accounts solve all these problems?

Local collection accounts eliminate or significantly reduce SWIFT intermediary deductions and improve settlement predictability. FX optimization depends additionally on the pricing infrastructure of your provider. Combined, the two significantly improve realized revenue.