Just last month, my neighbor Sarah lost $2,300 to a romance scammer who convinced her to send money through an untraceable method. This heartbreaking conversation made me realize how many people lack knowledge about the safest ways of sending money or understanding different secure transfer methods that protect our finances.

According to the Federal Trade Commission, fraud losses in the US reached over $8.8 billion in 2022, with the highest share coming from payment and money transfer scams. The truth is that most of these losses could have been prevented with proper knowledge about secure money transfer methods.

Having spent years working in financial security, I can share insights about protecting your money during transfers. Whether you’re sending cash to overseas relatives, paying for services, or handling emergencies, this guide will help you choose the safest methods of sending money.

Why Safe Methods of Money Transfer Matter More Than Ever

The digital age has revolutionized money movement, but it’s also created new vulnerabilities. Online money transfer security isn’t just about technology – it’s about understanding the entire ecosystem that protects your transactions.

The Hidden Dangers of Modern Money Transfers

Money transfer fraud has evolved beyond stereotypical email scams. Today’s scammers use sophisticated psychological tactics combined with seemingly legitimate platforms. From my investigation of hundreds of fraud cases, I’ve learned:

Romance scams now account for the highest individual losses, with victims losing an average of $4,400 per incident. Scammers build relationships over months before requesting money through untraceable methods.

Business email compromise attacks target individuals and small businesses, requesting wire transfers to “updated” account details that actually belong to criminals.

Fake emergency scams exploit our desire to help family members, with callers impersonating relatives in distress and demanding immediate transfers.

What Makes a Transfer Method Truly Secure?

Not all secure transfer methods are created equal. Through my research, I’ve identified five critical security elements:

- Regulatory oversight – Legitimate services operate under strict government supervision

- Insurance protection – Your money should be protected if something goes wrong

- Fraud monitoring – Advanced systems detect suspicious activity in real-time

- Identity verification – Both parties should be properly authenticated

- Dispute resolution – Clear processes for recovering funds when problems arise

Master Comparison: Best way to send Money safely

| Method | Security Level | Speed | Average Cost | Best For | Insurance Coverage |

|---|---|---|---|---|---|

| Bank Wire Transfers | Excellent | 1-3 business days | $15-50 | Large amounts, official payments | FDIC protected up to $250,000 |

| Digital Wallets (PayPal, Apple Pay) | Very Good | Instant | Free-3% | Online purchases, friends | Varies by platform |

| Money Transfer Services (Wise, Remitly) | Very Good | Minutes to hours | $2-25 | International transfers | Limited coverage |

| P2P Apps (Venmo, Zelle) | Good | Instant | Usually free | Splitting bills, family | Bank-level for linked accounts |

| Cryptocurrency | Variable | Minutes | $1-20 | Tech-savvy, privacy-focused | None |

| Cash Services (Western Union) | Good | Minutes | $5-50 | No bank account needed | Limited |

Traditional Banking: The Fort Knox of Money Transfers

1. Bank Wire Transfers – Maximum Security for Important Payments

When I need to send large amounts or handle critical payments, bank wires remain my top choice. Here’s why they’re considered the gold standard:

- SWIFT Network Protection: International wires use the Society for Worldwide Interbank Financial Telecommunication (SWIFT) network, processing over 42 million messages daily with bank-grade security protocols. Every transaction is encrypted, authenticated, and tracked through multiple verification points.

- Regulatory Compliance: Banks must comply with anti-money laundering (AML) and Know Your Customer (KYC) regulations. This means extensive verification processes that provide crucial fraud protection.

- FDIC Insurance: Your funds are protected by federal deposit insurance throughout the transfer process. If your bank fails during transfer, you’re still covered up to $250,000 per account.

However, wires aren’t perfect. They’re expensive, relatively slow, and nearly impossible to reverse once sent. I only recommend them for amounts over $1,000 when maximum security is essential.

2. ACH Transfers – The Unsung Hero of Secure Transfers

Automated Clearing House (ACH) transfers are one of the most secure and cost-effective ways to move money domestically. The ACH network processed 29.1 billion transactions worth $72.6 trillion in 2021, making it the backbone of the U.S. payment system.

What makes ACH transfers secure?

- Federal oversight by the National Automated Clearing House Association (NACHA)

- Batch processing allows additional fraud screening

- Reversibility within specific timeframes if fraud is detected

- Low cost – often free or under $3 per transfer

I use ACH transfers for regular payments like rent, utilities, and recurring transfers to family members. They’re not instant, but the security and cost benefits make them ideal for planned transactions.

Digital Payment Platforms: Modern Security Meets Convenience

1. PayPal – The Pioneer That’s Still Leading

PayPal processes over 22 billion transactions annually, with an impressive security track record. What sets PayPal apart in fraudproof payment options:

- Buyer and Seller Protection: PayPal’s protection programs cover eligible purchases up to the full amount, including shipping costs. I’ve personally used this protection twice for online purchases, and the resolution process was straightforward.

- Advanced Fraud Detection: PayPal uses machine learning algorithms to analyze hundreds of data points for each transaction, flagging suspicious activity in real-time.

- Two-Factor Authentication: Always enable 2FA on your PayPal account. This simple step prevents 99.9% of automated attacks, according to Microsoft’s security research.

Best practices for PayPal security:

- Never send money as “friends and family” to strangers (you lose protection)

- Always verify recipient email addresses carefully

- Use PayPal’s official app or website, never third-party platforms

- Enable account alerts for all transactions

2. Peer-to-Peer Apps – Convenience with Cautions

Apps like Venmo, Zelle, and Cash App have revolutionized how we split bills and send quick payments. However, their convenience comes with security trade-offs you need to understand.

- Zelle’s bank integration provides excellent security for transfers between verified bank accounts. Since it’s built into most major banking apps, it inherits your bank’s security infrastructure. However, Zelle transfers are instant and nearly impossible to reverse, making them attractive to scammers.

- Venmo’s social features can be a security risk. By default, your transactions are visible to friends, potentially exposing spending patterns. Always set your Venmo transactions to private and be cautious about transaction descriptions.

- Cash App’s Bitcoin features add complexity and potential security risks. While the app itself is secure, Bitcoin transactions are irreversible and can be challenging to trace.

My P2P app security rules:

- Only send money to people you know personally

- Verify recipient details through separate communication channels

- Keep transaction amounts reasonable (under $500)

- Enable all available security features (PIN, biometrics, etc.)

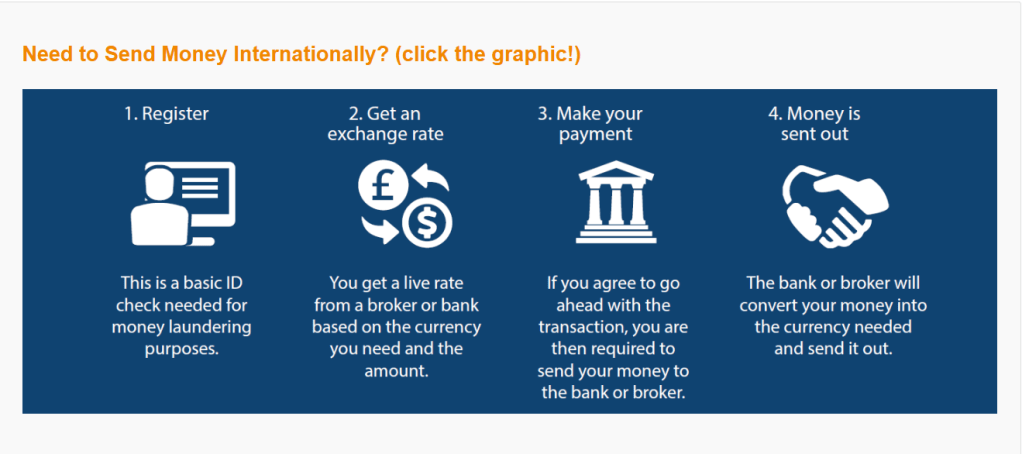

Global Money Transfer: Specialized Services for International Security

Wise (Formerly TransferWise) – Transparency and Security Combined

For foreign money transfer, Fairexpay needs Wise has become my preferred platform. Their transparent fee structure and robust security measures make them ideal for regular international transfers.

What makes Wise secure:

- Real exchange rates with no hidden markups

- Regulated in multiple jurisdictions, including the UK’s Financial Conduct Authority

- Segregated customer funds are kept separate from company assets

- Two-factor authentication and biometric login options

Wise’s borderless account functions like a multi-currency bank account with local account details in multiple countries. This eliminates traditional wire transfer risks by creating domestic transfers on both ends.

Remitly and Other Specialists – Security for Specific Corridors

Remitly focuses on specific transfer corridors, often providing better security and lower costs for transfers to developing countries. Their compliance with local regulations in recipient countries provides additional protection.

Key security features

- Local partnerships with banks and cash pickup locations

- Real-time tracking throughout the transfer process

- Identity verification using government databases

- Insurance coverage for transfers in transit

For global money transfer needs, I always recommend checking if specialized services serve your specific corridor before defaulting to traditional options.

Red Flags and Scams: How to Spot Unsafe Transfer Requests

Common Money Transfer Scams That Target Everyone

Romance scams remain devastatingly effective because they exploit emotions over months or years. The pattern is always similar: initial contact through dating sites or social media, gradual relationship building, eventual claims of emergency or travel needs, and requests for money through untraceable methods.

Overpayment schemes trick victims by sending fake checks or payments for more than owed, then requesting the difference be returned via wire transfer or gift cards. The original payment later bounces, leaving victims responsible for the full amount.

Tech support scams convince victims their computers are infected, then request payment for unnecessary services through methods that can’t be reversed.

Warning Signs of Unsafe Transfer Methods

Immediate red flags:

- Requests for gift cards, prepaid cards, or cryptocurrency only

- Pressure for same-day transfers without proper verification

- Requests to bypass normal security procedures

- Vague or changing explanations for why money is needed

- Recipients who refuse to provide proper identification

Always verify the recipient’s identity through independent means before sending money. A quick phone call to a known number can prevent most scams.

Step-by-Step Guide to Executing Secure Transfers

A. Pre-Transfer Security Checklist

Before initiating any transfer, I follow this systematic approach:

Recipient Verification:

- Confirm identity through independent communication.

- Verify the bank account or pickup details separately

- Check that the recipient’s name matches the official ID

- Understand exactly why the money is needed

Transfer Method Selection:

- Choose an appropriate security level for the amount

- Consider time sensitivity vs. security trade-offs

- Verify all fees and exchange rates upfront

- Ensure you have proper documentation

Amount Considerations:

- Stay within daily/monthly transfer limits

- Consider breaking large amounts into smaller transfers

- Keep records of all transaction details

- Plan for potential delays or complications

B. During Transfer Security Protocols

Network Security:

- Always use secure Wi-Fi or cellular data, never public Wi-Fi

- Verify website URLs are correct (look for https://)

- Clear browser cache and cookies after completing transfers

- Use official apps downloaded from legitimate app stores

Information Protection:

- Never share login credentials or verification codes

- Double-check all recipient details before confirming

- Save confirmation numbers and receipts immediately

- Take screenshots of transaction confirmations

Post-Transfer Monitoring

Track Your Transfer:

- Monitor the transaction status regularly

- Set up notifications for status changes

- Contact customer service if delays occur

- Keep all documentation until the transfer is complete

Follow-up Security:

- Verify the recipient received the funds

- Check your accounts for any unauthorized activity

- Update your security settings if you notice anything suspicious

- Report any problems to both the service provider and your bank

Cost vs. Security Analysis: Finding the Right Balance

Hidden Costs of Unsafe Transfers

- Direct financial losses from fraud can be devastating, but the hidden costs are often worse. Identity theft resulting from compromised transfer information can take years to resolve and cost thousands in legal fees and credit repair.

- Time costs for resolving fraudulent transfers average 23 hours per incident, according to identity theft studies. This includes time spent with banks, law enforcement, and credit agencies.

- Emotional stress shouldn’t be underestimated. Fraud victims often experience anxiety, depression, and loss of trust that affects their willingness to use legitimate financial services.

When Premium Security Services Are Worth It

For transfers over $5,000, I recommend paying extra for enhanced security features:

- Escrow services provide neutral third-party holding for high-value transactions. While they add cost and complexity, they’re essential for major purchases or business transactions with unknown parties.

- Enhanced customer support can be crucial when problems arise. Premium services often provide dedicated phone lines and faster resolution times.

- Additional insurance coverage beyond standard protections can provide peace of mind for large transfers or international business transactions.

Regulatory Landscape: Understanding Your Protections

Federal and State Transfer Protections

The Consumer Financial Protection Bureau (CFPB) oversees most money transfer services and provides complaint resolution processes. Understanding your rights under federal law helps you choose legitimate services and recover funds when problems occur.

State money transmitter licenses ensure companies meet minimum financial stability and consumer protection requirements. Always verify that your chosen service is properly licensed in your state.

International regulations vary significantly by country. Services like FairExpay and other emerging platforms must comply with multiple regulatory frameworks when facilitating cross-border transfers.

Dispute Resolution and Recovery Options

Regulation E provides specific protections for electronic transfers, including error resolution procedures and liability limits. However, these protections don’t apply to all transfer types, making service selection crucial.

Chargeback rights for credit card-funded transfers provide additional protection layers, though they’re not available for all transfer methods.

Federal deposit insurance protects funds held by licensed money transmitters, but coverage varies by service and amount.

Expert Tips for Maximum Transfer Security

Advanced Security Techniques

Multi-channel verification involves confirming transfer details through separate communication methods. If someone emails requesting a wire transfer, call them at a known number to verify before proceeding.

Graduated security approaches match protection levels to transfer amounts and risk factors. Small amounts to known recipients require different precautions than large international business payments.

Documentation strategies include keeping detailed records of all transfers, including purpose, recipient verification steps, and follow-up communications.

Industry Insider Recommendations

After consulting with fraud investigators and financial security experts, these practices consistently prevent the most common transfer fraud:

Never rush important transfers. Scammers create artificial urgency to prevent careful consideration. Legitimate needs can usually wait a few hours for proper verification.

Use established relationships. Banks and services you already use provide better protection and easier problem resolution than new platforms.

Understand irreversibility. Wire transfers, cryptocurrency, and cash pickup services can’t be reversed once completed. Double-check everything before confirming.

Your Action Plan for Secure Money Transfers

Protecting your money during transfers isn’t complicated when you understand the fundamentals. Choose transfer methods that match your security needs, verify recipient details independently, and never rush important financial decisions.

Start by evaluating your current transfer methods against the security criteria outlined in this guide. Enable two-factor authentication on all financial accounts, and create a personal checklist for future transfers based on the recommendations that apply to your situation.

Remember Sarah’s story from the beginning? She now uses only verified, secure transfer methods and has helped several friends avoid similar scams. The knowledge you’ve gained here can protect not just your money, but also help others in your community stay safe.

Your financial security is worth the extra few minutes of verification and the small premium for proper protections. Choose wisely, transfer safely, and keep your hard-earned money where it belongs.

Frequently Asked Questions

What is the safest method to send money internationally?

For international transfers, bank wire transfers offer the highest security but at a premium cost. Wise and Remitly provide excellent security with better rates for most personal transfers. The safest method depends on your amount, destination, and urgency needs.

What is the safest method to send money internationally?

Online money transfer security has improved dramatically, but safety depends on choosing reputable, regulated services and following proper security practices. Legitimate platforms use bank-level encryption and fraud monitoring. Avoid services that lack proper licensing or have unclear fee structures.

How do I avoid scams when sending money?

Avoiding scams in remittances requires verification of recipient identity through independent means, understanding common scam patterns, and choosing transfer methods with proper protections. Never send money to someone you’ve only met online, and always verify emergency requests through separate communication channels.

Is it safe to use mobile apps for transferring money?

Mobile app safety depends on the specific app and how you use it. Encrypted payment platforms like PayPal, Zelle, and bank apps provide excellent security when used properly. Enable all security features, keep apps updated, and only download from official app stores.

What precautions should I take during a money transfer?

Essential precautions include using secure internet connections, verifying recipient details independently, keeping transaction records, monitoring account activity, and understanding the specific protections offered by your chosen service. Never share login credentials or verification codes with anyone.

How can I verify if a money transfer service is legitimate?

Check for proper licensing through state money transmitter databases, verify regulatory compliance with agencies like FinCEN, read customer reviews from multiple sources, and confirm insurance or protection coverage. Legitimate services display their licensing and regulatory information.

What should I do if I suspect I’ve been scammed?

Contact your bank and the transfer service immediately, file reports with the FTC and local law enforcement, document all communications and transactions, and monitor your accounts for additional unauthorized activity. Quick action improves chances of fund recovery.

Are cryptocurrency transfers secure for regular money transfers?

Cryptocurrency security varies significantly by platform and user knowledge. While blockchain technology is secure, cryptocurrency transfers are irreversible and lack traditional consumer protections. Insured money transfers through traditional services provide better protection for most users.

Leave a comment