Compare money transfers vs wire transfers. Explore differences in speed, fees, security, and best use cases for personal and business remittances.

Money Transfer vs Wire Transfer: Key Differences Explained (Complete Guide 2025)

Ever stood at a bank counter in Mumbai and felt lost trying to pick between a money transfer and a wire transfer for that overseas payment? Trust me, you’re not the only one. Last year, Indians sent more than 100 billion dollars out of the country, yet most of us still confuse the two options.

Having guided friends and clients through countless cross-border payments, I’ve seen the wrong choice eat into their budgets by thousands of rupees. So, in this simple guide, we’ll break down the ins and outs of money transfers versus wire transfers, helping you save both time and cash the next time you send money abroad.

Understanding Money Transfers and Wire Transfers

What Are Money Transfers?

Money transfers are online services that let you send cash around the globe without stepping inside a bank. Instead of relying on old banking rails, these apps and platforms use their own networks, often boosting speed and keeping fees clear upfront.

So, when I send 50,000 rupees from Bangalore to my cousin in London through Fairexpay online money transfer, they take that money into their safe system. After they swap the rupees for pounds at a good exchange rate, the cash lands in her UK bank account in one or two business days.

What Are Wire Transfers?

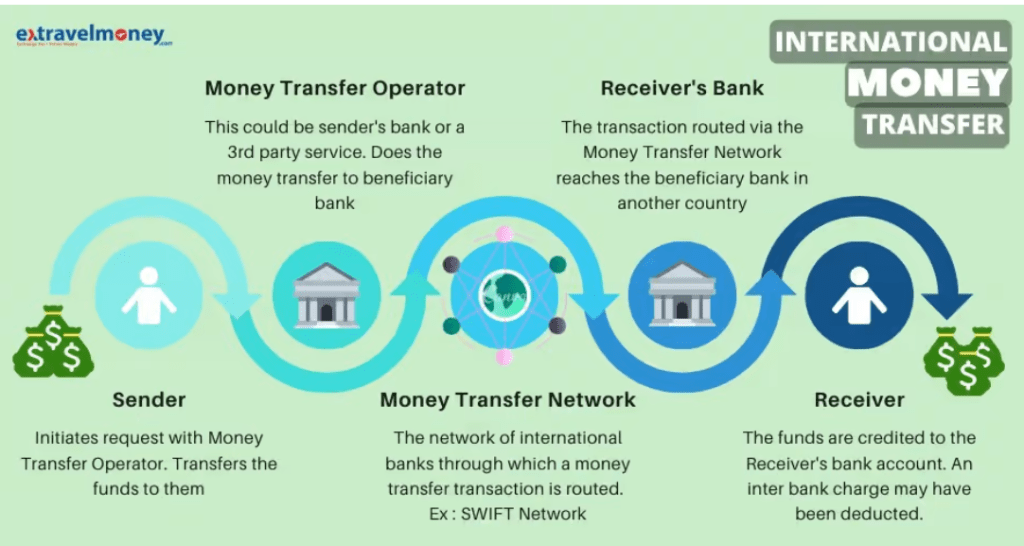

Wire transfers are the old-school way friends and families send money overseas, and they run on the SWIFT network. Your bank talks directly to the other bank through a secure private line, so this method feels solid and well tested.

Almost every Indian bank does wires, including:

State Bank of India

HDFC Bank

ICICI Bank

Axis Bank

Say I wire 1,00,000 rupees from my HDFC account to a US bank; the whole flow still rides on SWIFT. First, the bank checks the balance, then changes the cash into dollars, and finally tells the American bank to credit my friend’s account.

Money Transfer vs Wire Transfer: Complete Comparison

Factor

Money Transfer

Wire Transfer

Speed

1-3 business days

Same day to 2 days

Fees

₹200-₹800 per transaction

₹1,500-₹3,000 per transaction

Exchange Rates

Near mid-market rates

Bank rates with 2-4% margins

Convenience

Mobile apps, 24/7 online

Branch visits are often required

Transfer Limits

Up to ₹7,00,000 annually

Higher limits available

Documentation

Minimal for smaller amounts

Extensive paperwork required

Tracking

Real-time app updates

Limited bank notifications

Key Differences Between Money Transfer and Wire Transfer

1. Speed and Processing Times

Money-transfer apps usually finish an international send in 1 to 3 business days. In my own experience, companies like Xchange often get money to Europe in about 24 hours, while transfers to places like the Philippines or Mexico can take 2-3 days.

Wire transfers may edge out money transfers when time is critical. A domestic wire within India wraps up the same day, and an international wire generally clears in 1 to 2 business days. Just keep in mind that weekends and bank holidays can stretch that timeline.

Real Example: Last month, I had to send ₹75,000 right away to my daughter in Toronto. The wire hit her account in just 1 day, but I paid a total of ₹2,400 in fees. A money-transfer service would have taken 2 days and cost only ₹600.

2. Cost Structure Analysis

This is where money-transfer services and traditional wire transfers show their true colors. Most money-transfer apps have clear fees and decent exchange rates. When you send ₹1,00,000 to the U.S., for example:

Fairexpay: ₹550 plus whatever the market rate gives you.

Other popular services usually take between ₹600 and ₹1,200, depending on how fast you want the money to arrive.

Wires, on the other hand, pile on extra charges:

The bank first hits you with an outgoing fee of ₹1,500 to ₹2,500

Then there are correspondent bank fees of about $15 to $25

Once the cash lands, the receiving bank wants another $10 to $20

Finally, the currency mark-up can be 2 to 4 percent above the mid-market rate.

All told, sending the same ₹1,00,000 by wire ends up costing around ₹3,000 to ₹4,500, while a money-transfer route usually takes only ₹800 to ₹1,500, so the gap is clear.

3. Exchange Rate Differences

Because money-transfer companies rely mostly on small up-front fees, their exchange rates stay much closer to the real mid-market number. Fairexpay is one solid example; it shows the rate openly and cuts only a small fee on top. In contrast, banks that do wires typically pull extra profit from the currency spread. If the mid-market USD-INR rate is 83.00, a bank might give you only 81.50 or 82.00 and keep the gap alive as income. And that gap really adds up for larger amounts; if you send ₹5,00,000, a 2 percent drop costs you around ₹10,000, more than enough to cover several smaller transfers.

When to Pick a Money Transfer App Over a Wire Transfer

When to Use Money Transfer Apps

Money-transfer apps shine when you want to send smaller amounts on a regular basis:

Monthly family remittances below ₹2,00,000

Tuition fees or student living expenses

Small business buys from overseas suppliers

Transfers where saving money beats fast delivery

For example, Rajesh, an IT worker in Pune, sends ₹25,000 each month to help his parents in Kerala and support his brother studying in Germany. By using Fairexpay instead of a wire, he saves about ₹18,000 a year because of lower fees and a better exchange rate.

When Wire Transfers Make Sense

Wire transfers still rule in a few key situations:

Big business deals above ₹10,00,000

Same-day payments that can’t wait

Buying property when bankers require paperwork

Deals that play out best inside a bank’s network

Take Priya’s zero-room apartment down payment of ₹25,00,000 in Vancouver. Even with steep fees, she chose a wire because her Canadian bank insisted on official documents and demanded completion within 24 hours.

Money Transfer Apps vs. Banks in India

Top Digital Apps

Fairexpay

Pros: Good exchange rates, clear fees, easy-to-use app

Cons: Limitations in some sending or receiving countries

Best for: Budget-minded people who want safe overseas transfers

Other Digital Apps

Many other services give different rates, speeds, and extra features

Always check and compare what’s best for your own transfer

Classic Wire Transfer Banks

HDFC Bank

Fee: ₹1,500-₹2,000

Time: 1-2 days

Great for: Existing customers with premium accounts

State Bank of India

Fee: ₹1,000-₹1,500

Time: 1-3 days

Great for: Large transfers that come with lots of papers

Safety: Money App Transfers vs Wire Transfers

Both ways are safe if you stick to licensed, regulated firms. Transfers through apps follow RBI rules and keep their licenses current. Banks also obey strict SWIFT rules and global banking checks.

Money Transfer Security Features

End-to-end encryption

Two-factor authentication (2FA)

Alerts and tracking scans for fraud in real time

Transfers follow FEMA rules

Wire Transfer Security Features

Shielded by the SWIFT network

Bank-level security steps lock data

Verification happens at several stages

Every transfer leaves a clear audit trail

Warning Signs to Watch For

Unlicensed transfer agents

Offers that seem too good to be true

Hidden fees and weak customer support

Missing proof of regulatory approval

Legal Rules in India

Under the Liberalized Remittance Scheme, people can send up to $250,000, about 2.07 crore rupees, a year for approved reasons. This cap covers both money transfer apps and bank wires.

What you need to show:

For amounts under ₹50,000: Basic KYC papers

For amounts over ₹50,000: Purpose slip, income proof

For amounts above ₹7 lakh: Extra checks and documents

Tax bite:

TCS, or Tax Collected at Source, hits 5 percent on LRS remittances, rising to 20 percent in some cases.

Technology and Future Trends

The way we move money around the world is changing fast. New digital services are offering:

Near-instant transfers built on blockchain

Wallets that hold multiple currencies

AI tools that guess the best exchange rates

Easy links to UPI and other payments

Big banks are not sitting still; they are:

Building their own quick transfer apps

Teaming up with fintech startups

Cleaning up mobile banking screens

Speeding up back-end processing

Expert Tips for Choosing Between Money Transfer and Wire Transfer

To save money, always:

Look at the full cost, not just the fee

Add in how exchange rates cut or boost value

Think about how often and how much you send

Keep an eye out for promos or loyalty perks

When speed matters, you should:

Know the deadline for same-day service

Remember that weekends and holidays slow things down

Only pick the fast-track option when really needed

Whenever possible, plan your transfer a day ahead

For paperwork and rules, just:

Save a copy of every cross-border transfer

Know your purpose code and any limits

Keep receipts or contracts as backup

Ask a tax expert if the amount is big

Conclusion: How to Pick the Best Option for You

Choosing between the two really boils down to your situation. For sending pocket money to cousins, covering tuition bills, or any everyday move, a service like Fairexpay saves on charges and spice.

But when you must close on a house, fund a new factory, or finalize a merger, only a wire gives you the speed and signed proof, even if it costs more.

My simple tip: lean on money transfer apps for routine stuff and save wires for big, time-sensitive moves. Keep an eye on your yearly totals so you stay below LRS limits, and always add the real exchange rate to the final bill before pulling the trigger.

Whatever option you pick, money transfer or a wire transfer, stick with licensed providers that follow RBI rules and show their fees up front. Choosing the right company protects your cash and can save you money in a world where transfer options keep changing.

Frequently Asked Questions

1. What is the difference between a money transfer and a wire transfer? In simple terms, money transfers run on apps with clear fees, while wire transfers travel through banks and usually cost more. Expect a money transfer to hit you for ₹200 to ₹800, but a wire can take ₹1,500 to ₹3,000 or higher.

2. Which method is faster: money transfer or wire transfer? Wire transfers are usually the speedster for urgent needs, finishing in 1-2 days overseas and often the same day inside the country. Money transfer services take about 1-3 business days, but they usually have better rates and are more convenient if you don’t need the cash to arrive right this second.

3. Which has lower fees: money transfer or wire transfer? Money transfers almost always come with a lighter price tag. If you send 1,00,000 Rupees overseas, a money-transfer service will charge about 800 to 1,500 Rupees in total, while a bank wire can eat up 3,000 to 4,500 Rupees after you count all the fees and the mark-up on the exchange rate.

4. Are money transfers as secure as bank wire transfers? Sure, as long as you stick to licensed providers. Both follow the same big international security rulebooks. Money-transfer apps sit under RBI watch, use encryption, and the classic wire route runs over the secure SWIFT network. Go with regulators in either case, and you should be fine.

5. When should I use a money-transfer service instead of a wire transfer? Pick a money-transfer app when you send less than 2,00,000 Rupees regularly, when saving cash matters more than racing clocks, when you’re cool using a phone instead of a bank counter, and when the person getting the money has a bank account in a major country.

6. How is a wire transfer different from a money transfer when the amount is big? Wire transfers are set up to move large sums quickly, and banks issue the receipts needed for buying a house or closing a big deal. Although many money-transfer apps cap limits, they can still save serious cash even when the total reaches five figures.

7. Should I pick a money transfer or a wire transfer for business payments? If a small order arrives weekly or you pay several suppliers, money transfers cut fees and lend themselves to simple scheduling. On the other hand, a 50,000-dollar contract, an urgent payroll, or any transfer that needs a formal paper trail benefits from the speed and reliability of a wire.

Learn about the Income-Based Repayment (IBR) plan, eligibility, and how it helps manage student loan payments.

What is the IBR Plan? Income-Based Repayment Plan Explained (2025 Guide)

Drowning in student loan debt? Well, you’re not alone. Most students work part-time jobs while in school to help make ends meet; a study finds that the average graduate at a postsecondary level is $37,000 in debt. That’s no laughing matter and can create havoc when trying to manage finances monthly. This is where income-based repayment (IBR) plans come in and help borrowers repay their loans on terms that consider their income.

With my expertise aiding individuals in navigating the muddles of student loan repayments, it is clear that IBR has transformed the lives of millions. By reading this guide, you now have the power to understand everything concerning Income-Based Repayment plans – from the eligibility criteria to the years-long impacts of these plans.

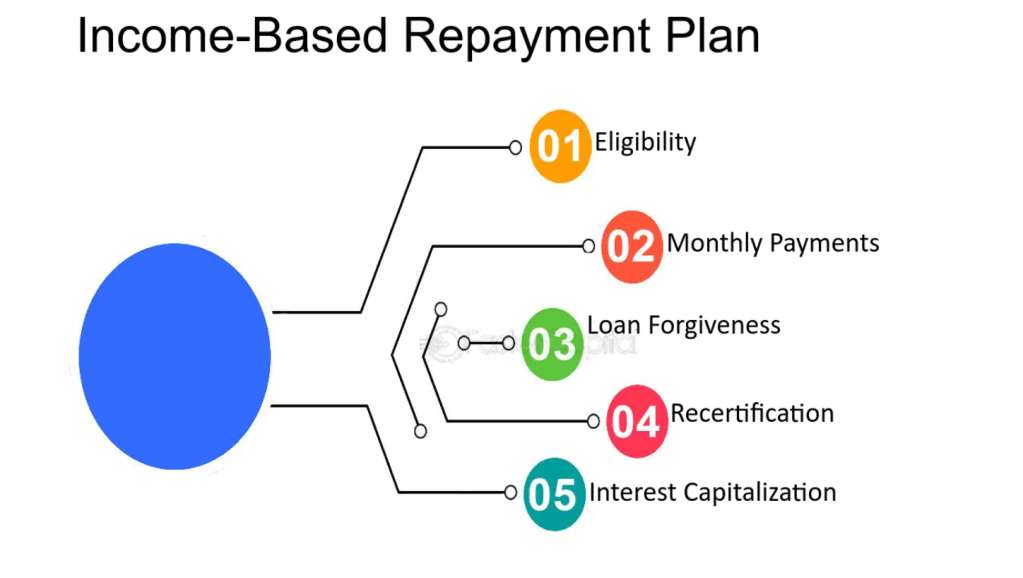

What Is IBR? Income-Based Repayment Plan Basics

The IBR Definition That Makes Sense

Income-Based Repayment (IBR) is a federally approved plan that allocates a student loan to be paid on a monthly basis, provided that the repayment portion does not exceed a certain portion relative to the income earned, along with separately considering the size of the family for every individual. In simpler terms, it assures to guard your finances against disbursement without taking control of your budget.

Unlike standard repayment plans, which are set to a generic repayment schedule, IBR is more accommodating and strives to shift the repayments to a fair, sustainable level based on the individual’s financial capabilities. Due to this uniqueness, IBR has surged in popularity among Americans.

How Income-Based Repayment Works?

And here’s the genius bit. IBR determines your payment based on a percentage of your discretionary income expenses. Your discretionary income is the difference between your adjusted gross income (AGI) and 150% of the federal poverty guideline for your household size.

The payment structure depends on when you first borrowed:

Original IBR: 15% of discretionary income (25-year forgiveness)

New Borrower IBR: 10% of discretionary income (20-year forgiveness)

Who is Eligible for IBR Plans?

There is, however, an eligibility criterion, and not everyone can jump on the IBR bandwagon. You need to show some degree of financial hardship, which means your IBR payment must be less than what you would pay under the standard ten-year repayment plan.

The positive news is that most holders of federal student loans qualify for them, particularly if you are:

A recent graduate with an entry-level job

Civic-minded service workers

Individuals going through a temporary financial hardship

Overspending parents

IBR vs All Other Income-Based Repayment Plans: The Definitive Distinction

Knowing your options is important. This is how IBR compares with other income-driven options:

Plan Type

Payment Rate

Forgiveness Timeline

New Borrower Date

Most Advantageous For

IBR (Original)

15% of discretionary income

25 years

Before July 1, 2014

Older borrowers

IBR (New)

10% of discretionary income

20 years

After July 1, 2014

Recent graduates

PAYE

10% of discretionary income

20 years

Requires partial hardship

Lower-income borrowers

REPAYE

10% of discretionary income

20/25 years

No hardship requirement

Graduate students

ICR

20% of discretionary income

25 years

No restrictions

Parent PLUS borrowers

When IBR Makes Perfect Financial Logic

From what I’ve seen, there are specific scenarios where IBR performs magic. You should strongly think about IBR if:

Your debt is more than 10% of your income

You intend to work in public service

You have a temporarily low income but have good growth potential

You require financial breathing room to stabilize your finances

IBR may seem unappealing to high-income earners who prefer to pay comfortably to standard payments, or those striving to lower total interest over the loan life.

IBR Eligibility Requirements: What Qualifies You?

Federal Student Loans Eligible Under IBR

IBR is limited to federal student loans. These include:

Direct Subsidized and Unsubsidized Loans

Direct PLUS Loans for Graduate Students

Direct Consolidation Loans

FFEL Program loans

Private education loans are not eligible for IBR, nor any other federal income-driven repayment plans. This highlights one of the key differences between federal and private loans.

Financial Hardship Criteria

Proving partial financial hardship is required to be eligible for IBR. In this situation, your IBR payment is less than the ten-year repayment plan amount.

As a simple illustration, if you’re required to make a standard payment of $350/month and your IBR payment is calculated at $200/month, you are eligible. The difference represents your financial hardship.

New vs. Original IBR: Understanding the Split

The two divisions of IBR stem from government changes:

Original IBR (borrowers before July 2014):

15% of discretionary income

Forgiveness in 25 years

Available to all eligible borrowers

New Borrower IBR (after July 2014):

10% of discretionary income

Forgiveness in 20 years

Exclusively for individuals without a federal loan history before July 1, 2014

How IBR Payment Calculations Work (With Real Examples)

Your Discretionary Income Formula

Discretionary income forms the foundation of IBR calculations. Here is the formula:

Discretionary Income = AGI – (150% × Federal Poverty Guideline)

For 2025, the federal poverty guideline for a single individual is $15,060, meaning 150% equals $22,590.

Step-by-Step IBR Payment Calculation

Allow me to illustrate with a case study:

Sarah’s Situation:

Annual income: $45,000

Family size: 1 (single)

Federal loan debt: $35,000

Post-2014 new borrower

Calculation Process:

Discretionary income = $45,000 – $22,590 = $22,410

IBR payment = $22,410 × 10% = $2,241 annually

Monthly payment = $2,241 ÷ 12 = $187/month

The previously mentioned standard monthly payment of around $350, when compared to the adjusted payments, highlights the reduced financial strain placed by IBR.

Payment Cap Protections

Here’s something crucial: IBR payments are capped at what you would pay on the standard 10-year plan. This protective feature ensures that you will not pay more than the capped amount, even if your income rises significantly.

The IBR Application Process: Your Step-by-Step Guide

Documentation Requirements Checklist

Before applying, ensure these documents are ready:

Last annual tax return or tax transcript

Last three months’ pay stubs

Document showing family size (marriage certificate or birth certificates)

Other income supporting documents (unemployment or disability payments)

Where and How to Apply for IBR

Options to apply are:

StudentAid.gov (most accessible and quickest)

The loan servicer’s website

Paper application sent to the appropriate loan servicer

Without a doubt, I prefer advising to go online. It’s the fastest, error-free method with instant confirmation of submission.

Expected Timeframes and What to Anticipate

Average processing duration: 2-4 weeks

During processing: Continue making your normal payments

Upon approval, the reduced payment amount will be implemented the following month

Pro tip: Apply well in advance. Do not wait until you’re already feeling the financial pressure.

Annual IBR Recertification: Stay on Track

An Annual Milestone That Must Not Be Overlooked

Every year, you are required to recertify your income and household size. Your loan servicer begins sending notifications 60 days prior; however, the responsibility still rests on you.

Failure to meet recertification deadlines incurs penalties, including:

Returning to standard payments of the 10-year repayment plan

Adding unpaid interest capitalization to the principal balance

Losing IBR benefits until recertification is achieved

Essential Documents Needed for Recertification

Documents needed include:

Updated tax returns from the previous year

Recent pay stubs (if employment has changed)

Family structure documentation for any changes

Confirmation of employment status

These processes can be streamlined through online portals, resulting in submission windows of 10-15 minutes; however, neglecting to submit can have dire consequences.

IBR Loan Forgiveness: Light at the End of the Tunnel

Understanding the IBR Forgiveness Mechanism

The balance owing is forgiven after the borrower has made qualifying payments for 20-25 years (depending on your version of IBR). All forgiven balances, including unpaid principal and accrued interest, will be discharged.

Qualifying payments include:

Payments made under IBR

Payments made under other income-driven repayment plans

Economic hardship deferment periods (not exceeding three years)

The Tax Bomb You Need to Know About

Here’s the catch: under IBR repayment plans, the forgiven debt is treated as taxable income. So if $30,000 is forgiven, you will pay taxes as if that amount was added to your income.

Example: If $30,000 is forgiven and you’re in the 22% tax bracket, you’d owe approximately $6,600. This “tax bomb” can cause significant financial stress if unprepared.

Planning strategies:

Set aside funds for taxes in a separate account

Consider paying over the minimum to lessen the amount forgiven

Determine eligibility for Public Service Loan Forgiveness (PSLF) and pursue it if applicable

IBR Pros and Cons: Complete Analysis

Major Benefits of Income-Based Repayment

Immediate financial relief: Reduced monthly obligations free up funds for other priorities

Flexible payment adjustments: Payments adjust automatically with income changes

Eventual loan forgiveness: Full discharge available after 20-25 years

Unemployment protection: During difficult circumstances, payments can drop to $0

Interest subsidy: The government pays part of your interest in some cases

Potential Drawbacks to Consider Carefully

Higher total interest costs: Lower payments over extended periods equal increased interest expenses

Extended repayment term: 20-25 years, opposed to a 10-year standard term

Annual recertification burden: Administrative tasks and deadlines every year

Tax implications: Forgiven debts are treated as taxable income

Greater complexity: More complicated compared to straightforward repayment plans

Real-World Case Study: Maria’s IBR Journey

With a bachelor’s degree in hand, Maria had $45,000 in federal student loan debt and worked as a social worker earning $38,000 yearly. She was estimated to pay $460/month on a standard repayment plan, which was not budget-feasible considering her income.

With IBR:

Monthly payment: $127

Extra cash flow: $333/month

Savings were utilized for an emergency fund and professional development

After five years, Maria’s income increased, but her payments remained manageable

“IBR gave me breathing room to build my career without drowning in debt,” Maria shared. “I had the option of taking a lower-paying job within my field instead of abandoning my passion.”

IBR During Major Life Changes

Marriage and IBR: What Changes?

Marital status does change your IBR calculation, but how you file taxes impacts it far more:

Married Filing Jointly: Both spouses’ incomes are used for payment calculation

Married Filing Separately: Only your income qualifies; however, you forgo specific tax advantages

Many couples prefer filing separately even when it increases their overall tax burden, as it keeps IBR payments lower.

Job Loss and IBR Protection

In the event of job loss, IBR offers critical protections:

Notify your servicer of your income change immediately

Payments could scale down to $0 with no earnings

Unemployment compensation is considered income for IBR calculations

An updated payment calculation can be requested at any time

Income Changes: When to Update

With significant improvements or reductions in income, you don’t have to wait for annual recertification. Contact your servicer if:

Your employment status changes (including pay cuts)

Your income increases by more than 10%

Your household size changes due to marriage, divorce, or children

IBR Success Stories and Common Mistakes

Success Story: From Overwhelmed to Empowered

James, a nonprofit worker, was managing a student loan payment of $520/month alongside a $60,000 salary. Upon switching to IBR, his payment decreased to $180/month.

“The additional $340 per month transformed my life,” James explained. “It allowed me to finally save for emergencies, contribute to my 401(k), and even budget for a vacation. IBR didn’t just help with my loans—it improved my entire financial picture.”

Common IBR Mistakes That Cost Money

Mistake 1: Missing recertification deadlines. Solution: Set calendar reminders 90 days before the deadline

Mistake 2: Failing to report changes in family size. Solution: Notify the servicer immediately when you marry, divorce, or have children

Mistake 3: Ignoring payment cap benefits. Solution: Understand that payments won’t exceed the 10-year standard amount

Mistake 4: Overlooking tax consequences. Solution: Start saving to cover potential tax liability on forgiven debt

Getting Started with IBR Today

Your Immediate Action Plan

Step 1: Contact your loan servicer to check IBR eligibility. Step 2: Collect necessary documentation (tax returns, pay stubs, family info.) Step 3: Apply online at StudentAid.gov. Step 4: Set up autopay to receive a 0.25% interest rate reduction. Step 5: Mark your calendar for next year’s recertification

Professional Help Resources

If you require assistance with IBR:

National Student Loan Data System (NSLDS): Track all your federal loans

Non-profit credit counseling agencies: Budget and debt management

Tools and Calculators

Federal Student Aid Repayment Estimator: Compare all payment options

IBR Payment Calculator: Estimate your monthly payment

Loan Simulator: Model different scenarios and strategies

Conclusion: For federal student loan borrowers facing burdensome monthly payment obligations, Income-Based Repayment can provide crucial financial relief. While IBR has its shortcomings—it increases total interest costs and requires ongoing maintenance—it offers flexibility and eventual forgiveness that can make the difference between financial stability and overwhelming debt.

Be strategic and analyze scenarios, evaluate your career path, and consider long-term implications before committing to IBR. When deployed with precision, it becomes a powerful tool that has enabled millions of borrowers to regain control of their student loan debt and build stronger financial futures.

Frequently Asked Questions

Who qualifies for IBR?

You qualify for IBR if you have eligible federal student loans and demonstrate partial financial hardship. This means your IBR payment would be less than your standard 10-year payment. Most borrowers with federal loans qualify, particularly those with entry-level incomes or large debt loads.

How is the monthly payment calculated under IBR?

IBR payments are calculated as either 10% or 15% of your discretionary income (income minus 150% of the federal poverty guideline), divided by 12 months. New borrowers after July 1, 2014, pay 10% with 20-year forgiveness, while earlier borrowers pay 15% with 25-year forgiveness.

Does IBR affect my credit score?

IBR itself doesn’t directly impact your credit score. However, making consistent on-time IBR payments will help build a positive payment history. If you were previously missing payments before switching to IBR, the lower payments can help you get back on track and improve your credit over time.

Can I switch from another repayment plan to IBR?

Yes, you can switch to IBR from any other federal repayment plan, including standard, graduated, or other income-driven plans. Contact your loan servicer to request the change. You’ll need to complete an application and provide income documentation, just like a new IBR applicant.

What happens if I miss my IBR recertification deadline?

Missing your recertification deadline causes your payment to revert to the standard 10-year amount, and any unpaid interest gets capitalized (added to your principal balance). You’ll need to complete the recertification process to restore your IBR benefits. Set calendar reminders to avoid this costly mistake.

Can I make extra payments while on IBR?

Absolutely! Making extra payments while on IBR can significantly reduce your total interest costs and help you pay off loans faster. Specify that extra payments should go toward principal, not future payments, to maximize the benefit.

How does IBR work with loan consolidation?

If you consolidate your loans through a Direct Consolidation Loan, you can apply for IBR on the new consolidated loan. However, consolidation resets your payment count for forgiveness purposes, so consider the timing carefully if you’re close to the 20-25-year forgiveness mark.

Discover what a Guaranteed Investment Certificate (GIC) is, how it works, and why it’s a safe investment option.

What Is a GIC? Guaranteed Investment Certificate explained: Your 2025 Complete Guide on Investment Certificates.

In this scenario, suppose you have $10,000 saved in a savings account earning an astonishing 0.5 percent interest per annum. The rate is so low that it does nothing to outrun inflation, let alone grow your savings. Does this ring a bell? Right, it does for most people. Luckily, there is an effective way to Secure Investment Certificates that utilize money lost in value due to inflation. GICs are one of the safest investment options in Canada, and earn decent rates of return, making them an attractive option.

GIC is very simple and complicated at the same time; here’s a full guide breaking down everything you need to know from comparison of top providers, understanding what Guaranteed Investment Certificates are, GIC withdrawal rules, along other important decisions around GICs.

Knowing the bank acronyms can be quite overwhelming, and so GICs need a thorough explanation because the Bank also considers GTD (Guaranteed Time Deposit) to be synonymous, and thus will treat both interchangeably.

What Is a Guaranteed Investment Certificate (GIC)?

A Guaranteed Investment Certificate (GIC) is essentially a loan you give to a financial institution in exchange for guaranteed interest payments. Consider it a formal IOU where your bank pledges to return your base principal in addition to some specified interest after a set period.

In essence, the process works as follows: you place a deposit with a bank, a credit union, or a trust company for a specific period known as the GIC maturity period. During this time, the deposit continues to earn interest at either a fixed or variable rate. Upon the expiration of the term, the initial capital, along with all earned interest, is paid back.

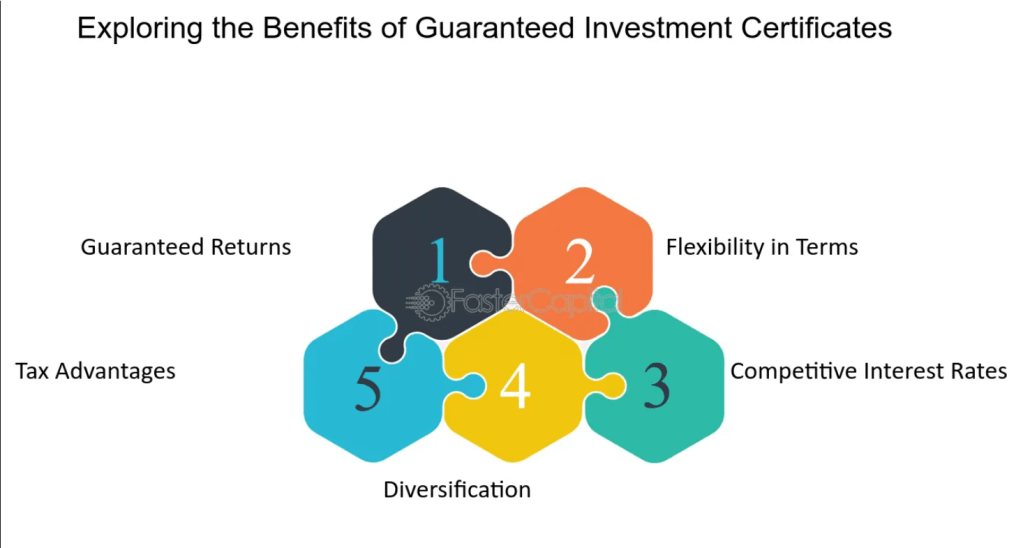

Key Benefits of GICs

Benefits that make GICs attractive include:

Principal protection: The original investment is guaranteed 100 percent

Predictable returns: Exact profit figures can be derived

CDIC insurance: Protecting funds up to $100,000 per institution

No management fees: Unlike mutual or exchange-traded funds

Flexible terms: Spanning from 30 days to 10 years

Embracing greater simplicity makes GICs more appealing relative to other forms of securities. Their resilience towards market fluctuations is attractive – if a stock market crash occurs or bond defaults, your GIC will remain unaffected, providing the original capital along with interest. This makes them particularly helpful for conservative investors who prefer lower, but guaranteed yields.

Types of GICs

Fixed-Rate GICs

Standard fixed-rate GICs are the most traditional and easiest to understand. They are akin to a simple flavor of ice cream – classic yet dependable. Fixed-rate GICs allow locking in interest for the whole term, ensuring that you will make money regardless of wider economic conditions.

As of now, the fixed-rate GIC interest rates sit between 2.5% and 4.8%, varying by the institution and term length. As a general rule, longer terms provide greater rewards in the form of higher interest rates.

Cashable vs Non-Redeemable GICs

The withdrawal policies for GICs become increasingly important at this juncture. Cashable GICs allow one to withdraw their funds before the agreed-upon time, although doing so will come at a cost of lost interest. Non-redeemable GICs provide higher interest rates, but in exchange, the funds are permanently locked away.

Comparison of Cashable vs Non-Redeemable GICs

Feature

Cashable GIC

Non-Redeemable GIC

Interest Rate

2.0-3.5%

3.0-4.8%

Early Access

Yes (usually after 30-90 days)

No

Rate Guarantee

Lower guaranteed rate

Higher guaranteed rate

Best For

Emergency funds

Long-term savings

Market-Linked GICs

If you’re looking for guaranteed principal protection but expect higher returns, market-linked GICs can be a suitable option as they offer stock-market-linked returns. While your principal is safeguarded, the interest earned is contingent on the performance of certain market indices.

How To Open A GIC Account – Step By Step

The procedure to open a GIC account is simple, but understanding the right way to open a GIC account can help save time while unlocking better rates at the same time.

Step 1: Research and Compare Rates

Look for the best deals from GIC providers in Canada. Big banks like RBC, TD, and Scotiabank have good deals, but better returns are often offered by credit unions and transfer money online.

Step 2: Gather Required Documents

You will need the following:

Government-issued photo identification document

Social Insurance Number

Proof of address

Funds for an initial deposit of $500 to $1,000, depending on the institution

Step 3: Choose Your GIC Features

Consider:

Term length: Match with your financial goals

Minimum deposit: $500 – $1,000, depending on the institution

Renewal options: Automatic renewal vs. manual decision

Step 4: Fund Your Account

Most organizations let you transfer funds from your bank account. Be cautious of the potential charges for transferring between banks.

(Tip: Review the money transfer charges list from your bank or provider to avoid unexpected fees and ensure the full amount reaches your GIC.)

GIC vs Fixed Deposit – Clarifying the Differences

Newcomers to Canada often ask about the differences between GICs and fixed deposits, especially if they are used to fixed deposits in other countries. While both these investments are considered low risk, there are some subtle differences:

GICs in Canada:

Have government and provincial regulations

CDIC insurance protection

Term option flexibility

Higher minimum investment requirements in most cases

Fixed Deposits (International Context):

Same idea, but different regulatory environment

Insurance for deposits may differ by region

Tax regulations may vary

Shorter minimum timeframes in many cases

Top GIC Providers – Where to Get the Best Rates

When choosing from the top GIC providers, you should look beyond the interest rates. Reliability, customer service, and competitive terms are equally important.

Leading GIC Providers in Canada:

Tangerine Bank: Competitive online rates and an easy-to-use platform

Meridian Credit Union: Member-centric, frequently offers the highest rates

Major Banks (RBC, TD, BMO): Convenient GIC options but often lower rates

Pro Tip: Don’t choose based on your current bank. Online and credit union institutions tend to offer 0.5-1% more than traditional banks.

Special Programs

Student GIC Program

Student GIC programs serve as educational funds and act as a requirement when applying for an international study visa. This particular GIC helps international students earn interest on the funds needed.

Key features of student GICs:

Minimum $10,000 investment

Funds are released gradually during studies

Acceptable for visa applications

Competitive interest rates

GIC Benefits for NRIs (Non-Resident Indians)

GICs for NRIs come with perks and benefits such as lower taxation and access to foreign currencies. These investments contain withholding taxation for NRIs that should be structured for maximum tax advantages; therefore, professional tax advice is recommended.

Tax Implications – What You Need to Know

GIC interest generates income and is taxed at your marginal rate. However, strategic placement can help counterbalance the overall tax liability:

Tax-Efficient GIC Strategies:

Hold GICs in TFSAs for tax-free growth

Use RRSPs for tax-deferred growth

Consider income splitting opportunities with your spouse

Time GIC maturities for optimal tax years

Annual tax reporting: A T5 slip showing the amount of interest earned is issued annually, regardless of whether the funds were received (for GICs paying interest at maturity).

Common Errors to Avoid

Having assisted numerous clients with their GIC investments, I have come across these errors time and time again:

Investing all funds into a single long-term GIC. This precludes you from taking advantage of higher rates should they become available. Consider GIC laddering, where you spread the investments over multiple maturity dates.

Ignoring inflation erosion. A GIC paying 3% sounds attractive until one realizes that inflation is at 3.5%. Always look at the inflation-adjusted value of returns.

Not understanding withdrawal terms. Some “cashable” GICs have restrictions or penalties that are not obvious. Always know the fine print.

Choosing convenience over returns. Banking where it’s easy might result in lost of interest of hundreds of dollars every year.

GIC laddering is the purchase of several GICs with staggered maturity dates. This ensures access to funds regularly while also earning good interest rates.

Example of a 5-Year GIC Ladder:

Year

Investment

Term

Interest Rate

Year 1

$10,000

1-year GIC

3.0%

Year 2

$10,000

2-year GIC

3.5%

Year 3

$10,000

3-year GIC

4.0%

Year 4

$10,000

4-year GIC

4.2%

Year 5

$10,000

5-year GIC

4.5%

After the maturity of the first GIC, renew into a fresh 5-year term. This approach maintains liquidity while capturing better long-term rates.

Conclusion – Is a GIC Right for Your Financial Goals?

Guaranteed Investment Certificates may not be the most exhilarating investments, but they fulfill crucial functions in diversified portfolios. They are ideal for your emergency funds, short-term savings objectives, or the conservative parts of your retirement planning.

Always assess your risk appetite, investment timeframe, and overall financial strategy before investing. GICs are most effective when you know what you will receive in return: absolute safety and reliable returns, albeit lower than stocks or other growth-oriented investments.

Remember, good investing practice is not about trying to identify the one perfect investment – it’s about creating a strategy that allows you to work towards your financial goals with minimal stress, providing peace of mind. Many Canadians find that GICs offer a balanced combination of safety and reasonable returns.

Would you like to explore other GICs? You may wish to start by assessing rates from various providers. It may also be helpful to consult a specialist to analyze the role of GICs in your overall investment strategy.

Frequently Asked Questions About GICs

What is a GIC?

You make a GIC through a deposit with a financial institution for a predetermined length of time. During this term, the financial institution pays you guaranteed interest for the use of your money. At the end, you get the money you deposited and the agreed interest on top.

Who should invest in a GIC?

A GIC would be suitable for conservative investors, elderly investors, people who are in the process of starting an emergency fund, or anyone who values the preservation of their funds over growth. It is also ideal for those investors who wish to avoid the stress of market fluctuations.

What is the risk profile of GICs?

The primary risks are:

Inflation risk: Gaining a return that doesn’t match rising economic costs

Interest rate risk: Missing out on higher rates if they rise post-investment

Liquidity risk: Funds are unable to be accessed for the entire term duration

Opportunity cost: Potential earnings lost due to funds not being available for other investments

Can I withdraw funds from a GIC before the term expires?

This depends on the type of GIC. For cashable GICs, early withdrawal is permitted but comes with penalties. For non-redeemable GICs, no early withdrawal is allowed except in extreme cases, like terminal illness, and even then, heavy penalties apply.

What happens in the event of a bank failure?

CDIC (Canada Deposit Insurance Corporation) protects your GIC up to $100,000 per institution. This means if your bank fails, you’re guaranteed a refund on the amount within the insured limit.

Are GIC earnings taxable?

Yes, GIC interest is considered taxable income. You will incur taxes at your marginal tax rate on interest income, regardless of whether it is paid out yearly or at maturity. However, GICs within a Tax-Free Savings Account (TFSA) grow tax-free, and those held in a Registered Retirement Savings Plan (RRSP) grow tax-deferred.

What’s the minimum amount needed to buy a GIC?

Most financial institutions have a minimum initial investment requirement between $500 to $1,000. Some may accept as low as $100. Increased funding often comes with better investment rates.

Should I choose fixed or variable rate GICs?

If interest rates are likely to fall or remain stable, fixed-rate GICs provide certainty and are more advantageous. Variable-rate GICs are beneficial in rising-rate environments, but add uncertainty about the total returns at maturity.

Step-by-step guide to sending money from India to other countries, covering methods, charges, and required documentation.

How to Send Money Abroad from India: Your Complete Step-by-Step Guide for International Money Transfers

Last month, I remember Priya, my friend from college, was trying to figure out a way to pay her son’s university fees in Canada. Priya used to go to a bank and wire transfer the money out there for years. She was losing out on thousands of rupees because of the bank’s exchange rates. Does this sound familiar?

In this guide, I aim to cover everything from Reserve Bank of India policies to the regulations that need to be complied with. This one-stop guide is perfect for anyone looking to transfer money internationally from India for education, support of family, business transactions, etc.

Understanding International Money Transfers: All You Need to Know

With everything under the Reserve Bank of India’s eye, India doesn’t make it easy when it comes to money transfers to foreign companies. Understanding these rules could mean a big difference between an unnecessary regulatory headache and a smooth transfer.

International money transfers from India include payments to overseas accounts, foreign companies, or individuals residing abroad. This covers:

Payment of the family

Business-related payments

Insurance premiums of overseas countries

Travel expenses

Tuition fees (within USD 10K)

Under the Liberalized Remittance Scheme (LRS), the Indian government permits its residents to transfer a specific amount of money abroad. Consider LRS as your yearly limit set for overseas transactions – currently pegged at $250,000 per financial year on a per capita basis. This cap is inclusive of everything, including education and purchasing of foreign properties, thus making it critical to map out your transfers strategically.

Primary Factors for International Remittances

As per the data from the RBI, Indians remit through legal means more than $18 billion every year. Notably, the main reasons are:

Education expenditure (40% of total remittance)

Family maintenance and support (25%)

Medical treatment overseas (15%)

Travel and tourism (12%)

Business-related activities (8%)

Having a clear rationale for the transfer helps in choosing the most suitable method and form of documentation needed.

Legal Framework: RBI’s Guidelines on Outward Remittance

The RBI guidelines for outward remittance form the foundation of the country’s foreign exchange regulatory framework in the country. These are not regulations for the sake of bureaucracy. They serve the purpose of providing certain equilibrium for the economy of the country while facilitating genuine cross-border interactions.

In the existing structure, any resident Indian can remit up to $250,000 in a single calendar year without requiring additional approvals. Nonetheless, this flexibility comes with certain limitations:

Transactions Permitted Include:

Visiting friends and relatives abroad

Remittance, either as a gift or a donation

Emigration

Seeking medical treatment

Pursuing education abroad

Maintenance of close relatives

Transactions Not Permitted Include:

Sponsoring contests or raffles

Gambling or any form of wagering

Foreign exchange dealings outside the country

Investment in companies engaged in the real estate business

The beauty of understanding these guidelines is how simple they are. Familiarity with the existing framework allows for seamless remittance. Too many have underestimated the rules and, as a consequence, have overthought legitimate remittances.

Required Documents According to RBI Guidelines

Documentation is essential for every international money transfer. Documents for outward remittance differ according to the amount of money transferred and the purpose behind it:

For Payments Less Than ₹25,000:

Purpose self-declaration

Current PAN card

Bank account information

For Amounts Exceeding ₹25,000:

Form A2 (declaration cum application)

CA certificate for amounts exceeding $50,000

Additional documents supporting the claimed purpose

Passport with Visa (if applicable)

Step-by-Step Guide: How to Send Money Abroad from India

I will present the entire process in simple steps. Based on my experience helping friends and family with international transfers, I can attest that being prepared alleviates the burden significantly.

Step 1: Determine Your Transfer Amount and Purpose

Before opting for any service, make sure to assess the amount of funds you will be transferring. This goes beyond choosing a principal amount; also, figure out the following:

Exchange rate volatility (can increase or decrease by 2-5% daily)

Service charges (₹500 to ₹2,000 for most providers)

Charges from intermediary banks (between ₹1,000 and ₹3,000 for telegraphic transfers)

Goods and service tax on transfer fees (18% on service fees)

As an illustration, when you send $10,000 for education, your total expenses will be somewhere between ₹8,50,000 to ₹8,80,000 based on your selection.

Step 2: Choose Your Transfer Method

Each option impacts an individual’s costs, speed, and convenience. Allow me to elaborate on what I’ve found for each option:

Traditional Bank Wire Transfers

While banks provide safety and an established method, they are costly. My bank charges ₹1,500 as a flat fee plus 0.25% of the amount being transferred. Exchange rates are 2-3% above the mid-market rate at best.

Online Money Transfer Services

Wise, BookMyForex, and Fairexpay are examples of online money transfer services that have changed how we send money from India abroad. These services have:

Better exchange rates

Lower fees

Transparent pricing

With a switch from traditional services to online services, I’ve personally saved over ₹15,000 each year.

Forex Cards vs Wire Transfers

The forex card vs wire transfer debate usually leaves people perplexed. While forex cards are optimal for travel-related purchases, wire transfers are suited for large, one-off payments like tuition fees or property purchases.

Step 3: Compare Costs and Services

Do not make a choice solely based on the advertised exchange rates. For an accurate assessment, utilize the following calculation:

Total Cost = (Amount × Exchange Rate) + Transfer Fees + GST + Intermediary Charges

Below is a simplified approach that I devised:

Get the mid-market rate from Google or XE.com

Identify the markup from each service offered

The sum total of all costs and charges

Evaluate the overall final amount disbursed

Money Transfer Methods: Detailed Comparison

Transfer Method

Processing Time

Typical Fees

Exchange Rate Markup

Best For

Bank Wire Transfer

2-5 business days

₹1,500-3,000

2-4% above mid-market

Large amounts, long-standing relationships

Online Services

1-3 business days

₹300-1,200

0.5-2% above mid-market

Regular transfers, cost-conscious customers

Forex Companies

1-4 business days

₹500-2,000

1-3% above mid-market

High value transactions, tailored service

Digital Platforms

Minutes to 24 hours

₹100-800

1-2.5% above mid-market

Fast access, smaller sums

NRI Money Transfer Options: Special Considerations

There is a stark contrast between NRI money transfer options and those for residents. For NRIs, they can:

Transfer any amount without restriction from NRE accounts

Utilize NRO accounts for restricted transfers (up to $1 million per year)

Benefit from a simplified documentation process

Access specialized NRI banking services

It’s a common misconception that NRIs have less flexibility than residents, when in fact, they are granted more flexibility for international transfers. This benefit may prove useful for decreasing spending during large-scale transactions.

Cost Optimization: Securing Low-Cost International Transfers

Achieving low-cost international transfers in India is not a simple process; rather, it is a clever strategy. Here’s what I have learned over the years while optimizing my international transfers:

Transfer Timing Strategy

The currency exchange rates are highly volatile and fluctuate at all times. I conveniently track the rates for USD-INR on tools like XE Currency and CurrencyFair. During the strengthening phase for the rupee, I execute planned transfers. During the weakening phase for the rupee, I delay non-urgent payments.

Pro tip: Do not attempt to transfer funds on Fridays or before long weekends, as these periods can attract weekend premiums, which add roughly 0.5-1% to your costs

Understanding Tax Implications

The tax on international transfers has undergone significant evolution over the years. Under the current framework, we operate with the following taxes:

TCS (Tax Collected at Source): 5% on the amount surpassing ₹7 lakh in a financial year under LRS

GST: 18% on the service fee for transferring money

Income tax: Based on the purpose of the transfer

For education, you can claim TCS as an advance tax, which is thus refundable. For other purposes, proper documentation aids tax optimization.

Choosing Speed vs Economy

While sending medical aid to my uncle in the US, I didn’t care much about the cost. However, I was willing to optimize my cost when it came to my daughter’s semester fees.

Fastest Ways to Send Money from India:

Digital wallets for certain corridors (2-4 hours)

Online transfer systems such as Wise (major currencies transfer within a day)

Express wire transfer (24-48 hours)

Most Economical Options:

Scheduled transfers booked in advance (saves 1-2%)

Bulk transfers for multiple payments

Forward contracts (rate locks on future transfers)

Specific Transfer Scenarios and Best Practices

Sending Money for Education

Tuition fees account for the majority of remittances sent from India. In helping many families with this, I learned several important methods.

Paying directly to the university is sometimes better than sending money to student accounts. A good number of universities will accept wires in INR and convert at more favorable institutional rates.

Documents Required for Educational Fund Transfers:

University offer letter

Document detailing fee categories and payment timelines

Student visa (where applicable)

Form A2 with CA authorization for amounts beyond $50,000

Family Maintenance and Support

Long-term automated support arranged via relationship banking frameworks streamlines regular family support payments. I automated monthly transfers for my parents’ maintenance expenditures in Canada, optimizing:

Standing transfer instructions, which provide enhanced value for repetitive transactions

Documented family member identification simplifies future transfers

Loyalty program benefits are granted after certain thresholds are met

Business and Investment Transfers

Corporate financial transactions require strict compliance protocols; however, they present particular beneficial aspects:

Increased transfer limits for authentic corporate purposes

Dedicated corporate banking facilities with lower fees

Multi-currency capabilities for international business activities

International remittance systems have been revolutionized by the ability to send money directly to bank accounts online. Convenience and lower costs are the main drivers behind the trend where more than 60% of outward remittances from India are processed electronically.

Mobile Applications and Online Platforms

Traditional banks are unable to compete with modern transfer apps because they offer:

Real-time rate alerts (get notified when rates hit your target)

Transfer tracking (know exactly where your money is)

Choosing solely based on advertised rates disregards total costs. Always calculate the final amount your recipient receives to avoid expensive surprises.

Conclusion

Transferring money from India doesn’t have to be costly or complicated. Strategic timing of your payments, selection of the appropriate service provider, and compliance with RBI guidelines can make this process significantly more cost-effective. You might save thousands of rupees annually with the right approach.

While a specific transfer method may work perfectly for your friend, it may not be optimal for your situation. Consider your specific circumstances, transfer frequency, acceptable risk levels, and various other factors when making decisions. Don’t hesitate to experiment with different service providers, as most offer first-time user discounts to test their services.

Frequently Asked Questions

What is the best way to send money abroad from India?

The best possible way varies between individuals. If you need regular transfers below $5,000, online money transfer services like Wise or BookMyForex would be efficient. For bigger amounts, specialized forex companies usually provide the best rates and personalized service. Traditional bank wire transfers work best when you have established relationships, despite expensive fees.

What documents are necessary for international transfers?

Document requirements differ based on the amount being transferred:

Less than ₹25,000: Self-declaration form along with PAN card

₹25,000 to ₹50,000: Form A2 along with purpose documentation, PAN card

Greater than ₹50,000: All documents mentioned previously plus CA certificate

Exceeding $250,000: Requires RBI approval

Always have your passport for identity verification and purpose documents (like university admission letters for education transfers).

Are there limits on how much I can send abroad?

Yes, under LRS for sending money abroad, residents are limited to $250,000 per financial year without special approval. This is a per-person limit, so married couples effectively have a cap of $500,000 annually. NRIs have more flexibility: unlimited from NRE accounts and up to $1 million per year from NRO accounts.

How long does it take to send money internationally from India?

Transfer times vary by method:

Digital platforms: 1-24 hours for major currencies

Bank wire transfers: 2-5 business days

Forex companies: 1-4 business days

Express services: Same day to 48 hours (with premium fees)

Transfers to developed countries (US, UK, Canada) process faster than developing countries due to superior banking infrastructure.

What is the tax on sending money abroad from India?

The existing taxation framework consists of:

TCS: 5% on LRS transfers above ₹7 lakhs annually (20% if PAN not provided)

GST: 18% on service charges

Income tax: Applicable depending on transfer purpose and income bracket

TCS on education and medical expenses qualifies as advance tax, hence it is refundable during tax filing.

Can I cancel an international transfer once initiated?

Cancellation policies differ by provider and transfer stage. Most services allow cancellation within 30 minutes to 2 hours after initiation. After processing begins, cancellation incurs fees (usually ₹500-2,000). Always check cancellation policies before confirming transfers.

Is it better to use a forex card or a wire transfer for international payments?

Forex cards are best suited for:

Travel expenses and daily expenditures

Multiple, smaller transactions

Countries with good card acceptance

Wire transfers are best suited for:

Large one-time payments (tuition fees, property purchases)

Direct bank-to-bank transfers

Countries with limited card infrastructure

How can I track my international money transfer?

Modern transfer services offer multiple tracking options:

SMS notifications at each transfer stage

Email updates with reference numbers

Mobile app tracking with real-time status updates

Customer service hotlines for instant updates

Preserving your transfer reference number is essential for tracking and customer service inquiries.

A complete guide to India’s Liberalised Remittance Scheme, including limits, eligibility, and uses for sending money abroad.

Liberalised Remittance Scheme (LRS): Your Comprehensive Guide to Sending Money from India in 2025

Imagine this: your son is applying for a college in Australia, and you need to send over ₹1.5 million for tuition fees. Or perhaps you’re taking a long-awaited vacation to Europe and plan to send money for hotel bookings. Whatever the reason, it’s common practice to know about LRS, but do you understand how it works?

Having helped a multitude of clients with forex services throughout India, I have come to understand that LRS is actually a well-kept secret and underutilized when used for transferring money internationally. Yet approximately 95% of the population barely scratches the surface of what it offers. From regulation changes to obsolete or expensive alternatives, this guide aims to streamline the process.

In this article, I will walk you through everything you need to know about LRS and how to implement it into your tax return. By the end, you will be fully empowered to utilize LRS and not suffer through unnecessary time delays.

What is the Liberalised Remittance Scheme (LRS)?

The Liberalised Remittance Scheme is relatively new in India’s economic landscape. It grants the resident population the privilege of sending money abroad with minimal regulatory hurdles. This scheme was introduced by the Reserve Bank of India (RBI) back in 2004 and revolutionized foreign exchange accessibility for Indians, as they could now obtain foreign currency without the traditional hassles.

Before the LRS scheme was introduced, remittances had to be sent after waiting for weeks of endless paperwork and RBI approvals. The scheme worked by allowing a streamlined process where Indian residents became eligible for a certain annual sum without the need for prior RBI approval.

Here’s what makes LRS unique: it covers nearly everything any user would expect, from using foreign currency to paying for university tuition, purchasing stocks, or even buying a second home in Dubai. The power lies in how uncomplicated this scheme is.

The LRS principles rest on simple assumptions of providing freedom to Indian residents for managing their foreign exchange transactions, with reasonable restrictions in place to reduce the chances of misuse.

Who is Eligible Under the Liberalised Remittance Scheme?

Understanding the eligibility criteria for LRS is important because getting it wrong could mean transaction rejections and delays.

Eligible Users:

Residents of India who are 18 years and older

PAN cardholders

Anyone who is a resident of India for tax purposes

Hindu Undivided Families (HUFs) with proper documentation

Important Note: Not all Indians are automatically eligible. The most crucial detail is residential status under the Foreign Exchange Management Act (FEMA); citizenship does not matter.

Who Does NOT Qualify:

Non-Resident Indians (NRIs)

Persons of Indian Origin (PIOs)

Registered firms, companies, and partnership firms

Trusts and societies

Minors (with some exceptions)

Many NRIs tend to get this mixed up. Residential status is what determines eligibility, regardless of holding an Indian passport. If you are an NRI, you will have to use different channels for remittances – LRS is not available to you.

The Evolution of LRS Limits

The most common inquiry I receive is, “What’s the annual limit under LRS?” Currently, for 2025, it remains $250,000 per financial year per individual. At today’s exchange rates, this amounts to approximately ₹2.1 crores, a considerable sum that fulfils most offshore financial requirements.

Current LRS Limits (2025-26):

Category

Per Person Limit

Family of Four Combined Limit

2025-26

$250,000

$1,000,000

Previous Years

$250,000

$1,000,000

Historical Evolution of LRS Limits:

2004: $25,000 (scheme launch)

2007: $50,000 (doubled)

2008: $100,000 (pre-financial crisis increase)

2013: $75,000 (temporary reduction due to economic slowdown)

2014: $125,000 (gradual recovery)

2015-2025: $250,000 (current stable limit)

The RBI has maintained the limit at a steady $250,000 for over seven years now. This stability shows the central bank believes this is the right balance between personal freedom and regulatory control.

What Transactions Are Permitted Under LRS?

The scope of transactions under LRS is vast, covering most reasonable needs for foreign exchange. Here are the key categories:

1. Education-Related Remittances

LRS for education is perhaps the most popular use case. Parents commonly use LRS to:

Pay university fees for children studying overseas

Support living expenses

GIC & Blocked account transfers

Rental payments

Real Example: Recently, we assisted a family from Mumbai whose son was pursuing a computer science degree in the US. The family was able to send approximately $45,000 throughout the year for education and living expenses, with funds accessible within one working day.

2. Healthcare Services Overseas

LRS accommodates medical emergencies and planned treatments:

Emergency medical treatment abroad

Specialized treatment procedures

Purchase of medical equipment

Medical travel expenses

3. Travel and Tourism

LRS for travel covers holiday and work-related expenses:

Hotel bookings and holiday packages

International flight tickets

Travel insurance policies

4. Investment Opportunities

Real estate investments outside India

International stock markets and exchanges

Foreign mutual funds and ETFs

Investments in gold and precious metals (where permitted)

5. Gifting and Family Maintenance

Support for relatives residing abroad

Wedding and celebration funding

Charitable contributions to registered foreign non-profits

6. Emigration & Employment

Work visa application fees and processing costs

Immigration lawyer and legal consultation fees

Skills assessment and professional qualification verification fees

Employment verification and background check costs

LRS Documentation Requirements

Incomplete submissions lead to delays, wasting both time and money. Proper preparation is key to avoiding these issues.

Primary Documents (Always Required):

Form A2 – the core LRS application form

PAN Card – mandatory for all transactions

Aadhaar Card – for identity verification

Purpose-specific supporting documents

Education-Specific Documents:

University Admission Letter

Visa (If available)

Passport

I-20/CAS (For US/UK)

Medical Treatment Documents:

Medical Invoice

Passport

Flight tickets

Visa

Travel Documents:

Invoice

Flight Tickets

Visa

Passport

Common Documentation Mistakes to Avoid:

Incomplete Form A2 – all fields must be filled correctly

Outdated documents – Expired Visa/Admission letter

Understanding Tax on LRS Remittances

Tax regulations on LRS remittances have evolved considerably, particularly regarding TCS (Tax Collected at Source) policies.

TCS can be claimed as a refund since it’s treated as an advance tax payment:

Report the TCS amount in your ITR

Offset against total tax liability

If TCS exceeds liability, initiate the refund process

Processing typically takes 4-6 months

Recent Changes and Updates

Key Updates 2024-25:

Enhanced Digital Processing – More remittance partners offer complete online LRS processing

Stricter Documentation Requirements – Enhanced reporting for certain transaction types

Clarified TCS Rules – Clearer guidelines on TCS exemptions

Budget 2025 Impact:

The latest budget has significantly revised LRS TCS provisions, easing the compliance burden on taxpayers. The TCS threshold for remittances under the Liberalised Remittance Scheme increased from ₹7 lakh to ₹10 lakh per financial year, effective April 1, 2025. TCS no longer applies to educational remittances funded through recognized financial institution loans. Despite this relief for overseas remittances, the government maintains strong enforcement measures in other areas to ensure tax compliance.

LRS Violations and How to Avoid Them

LRS violations can result in monetary penalties or legal action. Here are common mistakes and prevention strategies:

Common Violations:

Exceeding Annual Limits – Results in automatic rejection and RBI reporting

Multiple Bank Usage – Using different banks to circumvent limits

Maximizing LRS Benefits

Optimal Timing for Transactions:

Best Months: April-May (post-tax season stability) and October-November (pre-festive season)

Avoid: March (year-end volatility)

Strategic Planning:

Spread large transactions across the financial year

Monitor exchange rate trends

Plan documentation well in advance

Conclusion

The Liberalised Remittance Scheme represents financial freedom for Indian residents, the ability to engage globally while staying within regulatory frameworks. Whether funding your child’s overseas education, exploring international investments, or taking that long-awaited vacation, LRS provides the structure to achieve your goals.

Remember, effective LRS usage isn’t just about knowing the rules; it’s about optimizing them for your needs. Take transactions step by step, build relationships with your bank’s forex team, stay updated on policy changes, and most importantly, document everything meticulously for compliance and peace of mind.

With LRS as your tool and this guide as your roadmap, navigating international finance becomes significantly simpler. Your global financial journey starts with that first LRS transaction. Make it count.

Ready to begin your LRS journey? Start by organizing your documentation and contacting your bank’s forex department. A world of international opportunities awaits you.

Frequently Asked Questions

Who is eligible for LRS?

Indian residents aged 18 and above with valid PAN cards are eligible. This includes individuals and Hindu Undivided Families (HUFs). NRIs, companies, and minors are not eligible.

What is the annual limit under LRS?

The current limit for 2025 is $250,000 per individual per financial year. This limit resets every April 1st and cannot be carried forward.

What transactions are allowed under LRS?

Permitted transactions include educational expenses, healthcare costs, travel, overseas investments, family maintenance, gifts, and certain business consultancy services. Direct business investments and illegal activities are prohibited.

Do I need RBI approval for LRS transactions?

No prior RBI approval is required for LRS remittances within prescribed limits and for permissible purposes. However, proper documentation and reporting requirements must be followed.

Can I use multiple banks for LRS

While not legally prohibited, using multiple banks for LRS transactions within the same financial year is not recommended as it increases regulatory scrutiny and complicates record-keeping.

What happens if I exceed the LRS limit?

Transactions exceeding the $250,000 annual limit will be rejected. No further LRS transactions will be possible in that financial year, and amounts above the limit require special RBI approval.

How long does LRS processing take?

Complete online applications are typically processed within 1-3 working days. Branch submissions take longer, and incomplete documentation can cause additional delays.

Can I cancel an LRS transaction?

Yes, transactions can be cancelled before processing. However, once funds reach overseas accounts, cancellation becomes complex and may incur additional charges.

Understand cryptocurrency basics, how it works, and explore popular coins making headlines in the 2025 digital economy.

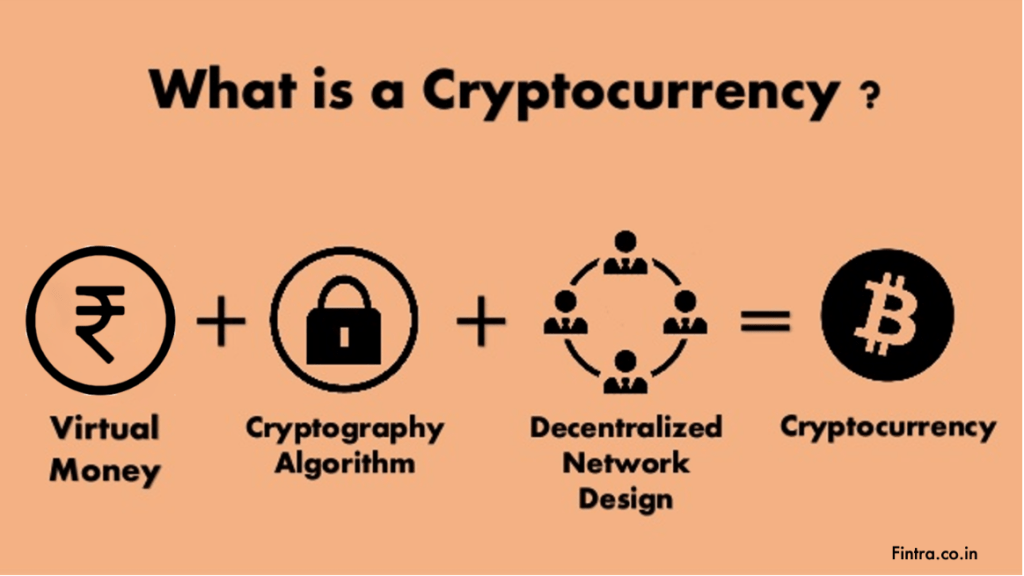

What is Cryptocurrency? Your Complete 2025 Guide to Digital Money Basics

Do you still remember the times when your grandparents would keep their cash savings under the mattress? The modern generation also saves their money, but not in the physical world. Their savings are found in virtual wallets only accessible in the digital realm. This is what cryptocurrency is all about. If you’ve been living under a rock and wondering about the reason behind the immense hype, rest assured that many others are like you.

Allow me to help you understand cryptocurrency at this stage. Of course, this guide will be helpful for people who are scared of jargon and technical terms too, so whether you are someone born yesterday just looking for some additional income through digital assets or someone with experience, there will be something for everybody.

Understanding Cryptocurrency -Basics of cryptocurrency Simplified

The Definition People Still Cannot Get Over

Cryptocurrency is something that can be understood as a new form of money. Consider it an internet phenomenon or manifestation of development. Like traditional currency, there is also a digital equivalent of it, which we talk about as “cryptocurrency.” It cannot be controlled or manipulated, unlike monetary funds.

This is the highlight of cryptocurrency:

Lacks a tangible aspect – Bitcoin cannot be grasped like a dollar bill would be languidly held

Loss of central oversight – no single authoritative body overseeing the cryptocurrency makes it more secure

Advanced mathematics can offer custody to your funds – cryptocurrency adopts an advanced systematic approach to secure funds.

Universal acceptance – limited only to regions that have the internet

Losing or having it confiscated isn’t a possibility, just like the digital dollar, bound by complex mathematical codes, it requires zero means of government backing.

How It Differs from Conventional Fiat Currency

When talking about cryptocurrency, a tweet comes to mind – the same way emails replaced letters, with more advantages, convenience, and quicker. Email dominates correspondence, and crypto is dominating the monetary terrain.

In the olden days, physical cash used to depend on governance. Crypto for beginners requires:

Approval of currency exchange and payments

Ensuring anti-money laundering

Secure the protection of funds

Credit card debt maintenance

Every single minute of the processes detailed above is done automatically through:

Systems placed miles away

Computer systems

Calculation of complex algorithms

Visible databases

Automated systems of approval

Now, sending money to a friend located in Tokyo is as simple as sending a text – no maintenance fees while transferring value.

Breaking Down Cryptocurrency By Using Blockchain Technology

Blockchain technology is central to the operation of any cryptocurrency. I prefer to think of blockchain technology as a ledger that stores information permanently and is duplicated millions of times around the globe on different computers.

Picture a scenario where a group of people (you and your friends) keep a note of debts in a physical notebook. Each time someone’s debt is settled (money owed is paid), a note is made in the notebook. Now say that this notebook:

Is replicated in all group members’ cellphones

Gets updated in real time as transactions occur

Cannot have transactions and their corresponding records removed or forged

Is transparent to all group members

This is precisely how cryptocurrency works – instead of friends having phones, we have thousands of computers maintaining all records.

How Does Cryptocurrency Work? The Complete Process Explained

Mining And Validation – The Network’s Security Guards

You could perhaps be thinking that such a system cannot be maintained with integrity. How do you ensure that this entire system is kept honest? With cryptocurrency mining, which, by the way, isn’t anything like gold digging.

Essentially, miners are digital accountants who:

Gather awaiting transactions from the network

Ensure each transaction is validated

Capture the block after resolving intricate mathematical puzzles

Add the confirmed block to the blockchain

Earning cryptocurrency as a reward for their efforts

In Bitcoin, new blocks are added roughly every ten minutes. This process is akin to having thousands of independent auditors verifying the same transaction – if there is a unanimous agreement, it is deemed valid.

Cryptocurrency Wallets: Your Money Storage Digitally

Consider a crypto wallet as a digital bank account. However, it differs in several key ways. Your wallet does not hold cryptocurrency directly (it’s data on the blockchain), rather it contains:

Your public address serves as an account number that can be viewed by others

Your private key is akin to a password and should remain confidential

Types of cryptocurrency wallets:

Wallet Type

Security Level

Convenience

Best For

Hardware Wallets

Highest

Low

Long-term storage

Software Wallets

Medium

High

Everyday transactions

Mobile Wallets

Medium

Highest

Quick-access payments while on the go

Web Wallets

Lowest

Highest

Beginners, small amounts

As an instructor, I advise students: do not ever share your private key. That would be like providing the PIN to your debit card, allowing unrestricted access to everything.

Transaction Process – From Click to Confirmation

Let’s take a closer look at the transactions involving sending cryptocurrency to someone:

The transference begins through the individual’s wallet application