Classifying FX losses as an operating cost is a structural mistake that hides the real problem. FX losses are not costs you incur — they are revenue you earned but never received. The distinction changes everything: who owns the problem, how you measure it, what you optimize, and ultimately, how profitable your export business actually is.

The Label Is Wrong, and It’s Costing You

Open any P&L statement for an Indian exporter and you’ll find a line called ‘Forex Loss’ somewhere in operating expenses. It sits alongside things like rent, salaries, and vendor payments. It gets treated as a cost of doing business — something to minimize where possible, but ultimately accepted as a feature of international trade.

That framing is wrong. And it’s worth examining carefully, because the label you use for a problem determines how seriously you take it, who you hold accountable, and what actions you’re willing to invest in to fix it.

Rent is a cost. You negotiate the lease, you sign it, you pay it. It’s a resource consumed in exchange for a service.

Salaries are a cost. People work, you compensate them. Fair exchange.

FX loss is different. You created value — you exported a service or good, you invoiced your buyer, your buyer paid you. The revenue was yours. Then, somewhere in the process of getting that money from their bank account to yours, a portion of it simply didn’t arrive. You didn’t spend it. You didn’t exchange it for something. It evaporated.

That’s not a cost. That’s lost revenue.

Why the Distinction Actually Matters

You might be thinking: isn’t this just semantics? Either way, the money is gone.

It’s not semantics. Here’s why the framing matters practically.

1. Ownership Changes

When FX is classified as a cost, it’s owned by the finance team as an accounting matter. It sits in the books. Someone reconciles it. Nobody urgently tries to eliminate it.

When FX is classified as lost revenue, it becomes a treasury and commercial problem. The question changes from ‘how do we account for this’ to ‘why aren’t we collecting what we earned.’ That’s a conversation that reaches the CFO, the business owner, the pricing team. Costs get managed. Revenue gaps get hunted.

2. Measurement Changes

Costs are measured against budget. If your forex loss is within budget, it’s fine.

Revenue is measured against potential. If you earned USD 300,000 but only realized USD 288,000, that’s a USD 12,000 revenue gap. The question becomes: what would it take to close it? That’s a different kind of urgency.

3. Investment Calculus Changes

Organizations will invest in revenue growth far more readily than in cost reduction. If switching payment infrastructure saves USD 6,000 per year, it gets compared against setup friction, switching cost, and finance team time. Often the math doesn’t win.

If switching payment infrastructure recovers USD 6,000 in annual revenue that was always yours, that’s a different conversation. The money already existed. You just weren’t capturing it.

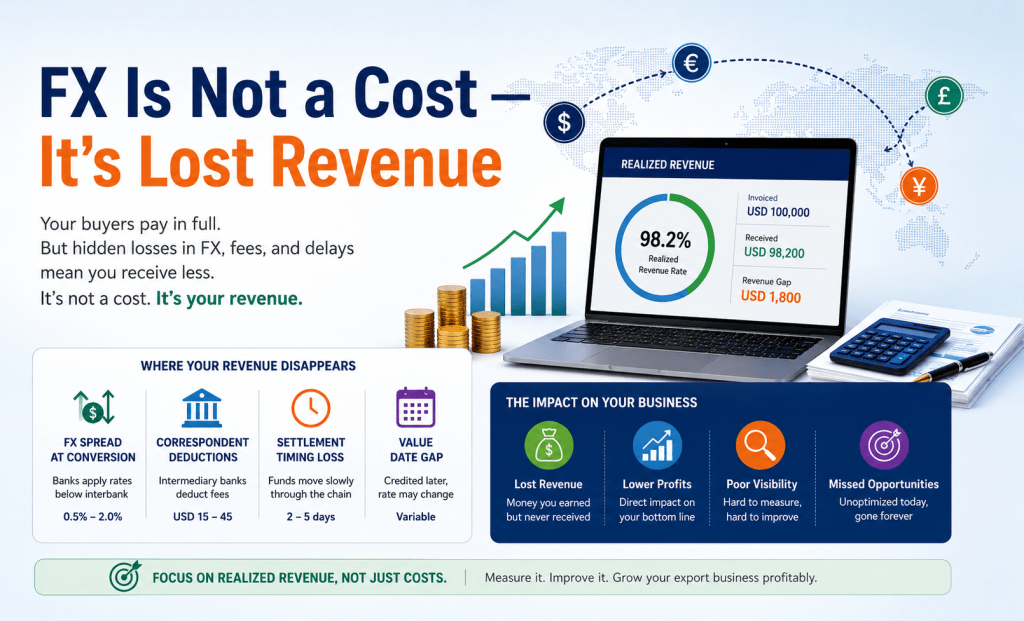

Where the Revenue Actually Goes

Let’s be specific. When an exporter sends a USD 50,000 invoice and ultimately receives INR equivalent to USD 48,200, the USD 1,800 gap is not random noise. It has a structure:

| Revenue Gap Item | Mechanism | Typical Impact |

|---|---|---|

| FX spread at conversion | Bank applies a rate less favorable than interbank market | 0.5%–2.0% of amount |

| SWIFT correspondent deductions | Intermediary banks deduct processing fees from your payment | USD 15–45 per transaction |

| Settlement timing loss | Payment sits idle in correspondent chain for 2–5 days | Indirect, working capital cost |

| Value date gap | Your account credited later than funds clear, affecting FX rate applied | Variable |

Each of these is a portion of revenue you created that didn’t survive the journey to your account. Not a cost you chose to incur. Not a service you’re receiving in exchange. Revenue that was earned but not captured.

How Realized Revenue Thinking Works in Practice

Businesses that treat FX as a revenue function — rather than a cost line — operate differently. Here’s what that looks like concretely.

- They measure realized rate per transaction, not just total INR received. On each payment, they know: what was the effective USD/INR rate we achieved? What would we have received at mid-market? The difference is tracked as realized revenue shortfall.

- They set a realized revenue target, not just an FX budget. Instead of ‘keep forex losses below 1.5% of receipts,’ they say ‘we should be realizing at minimum 98.5% of invoice value in INR equivalent.’ This shifts the frame from tolerance to expectation.

- They benchmark quarterly. Every three months, they review realized rate against the average mid-market rate for the same period. Consistent underperformance triggers action.

- They treat payment infrastructure as a revenue decision. When evaluating collection platforms, the question is not just ‘what does it cost’ but ‘what does it recover.’ A platform that charges a small fixed fee but offers transparent interbank FX pricing may recover significantly more revenue than a ‘free’ bank account with an opaque 1.5% spread.

The Numbers on a USD 25k+/Month Business

For an exporter collecting USD 300,000 per year:

| Scenario | Realized Rate vs Interbank | Annual Revenue Captured | Annual Revenue Gap |

|---|---|---|---|

| Current state (typical SME bank) | 98.0%–98.5% | USD 294,000–295,500 | USD 4,500–6,000 |

| With optimized FX infrastructure | 99.2%–99.5% | USD 297,600–298,500 | USD 1,500–2,400 |

| Improvement in captured revenue | ~1.0%–1.5% | USD 2,100–4,500 additional | — |

That USD 2,100 to USD 4,500 annual improvement requires no additional sales, no new clients, no pricing change. It simply requires treating the revenue capture function with the same rigor as the revenue generation function.

The Bigger Shift: From Transaction Thinking to Treasury Thinking

The core of this reframing is a shift from seeing international payments as a series of individual transactions to seeing them as a continuous revenue stream that needs to be actively managed.

Transaction thinking asks: did the payment arrive? Treasury thinking asks: what percentage of the revenue we generated is actually reaching our INR account, consistently, predictably?

For businesses at the USD 25k/month threshold and above, this distinction becomes increasingly material. Growth amplifies inefficiency. If you’re losing 2% of revenue to FX at USD 300k annual collections, you’ll lose the same 2% at USD 3 million. But the absolute number is now USD 60,000 per year — and that’s material enough to change how you’ve built your entire payment infrastructure.

The businesses that grow their export operations most profitably are the ones that make this realization early, not after they’ve scaled the problem.

Frequently Asked Questions

What is the difference between FX cost and FX revenue loss?

FX cost refers to explicit charges (like transfer fees or conversion fees) that appear on statements. FX revenue loss is the invisible gap between what you invoiced and what you realized — caused by bank spread, intermediary deductions, and rate differences. The distinction matters because revenue loss requires different tools to measure and different decisions to address.

What is realized revenue for exporters?

Realized revenue is the INR equivalent you actually receive from your international collections, expressed as a percentage of your invoice value. If you invoice USD 100,000 and receive INR equivalent to USD 97,500, your realized revenue rate is 97.5%. Tracking this consistently is the foundation of FX optimization for exporters.

How do you calculate FX leakage?

Compare the INR you received for each USD transaction against the INR you would have received at the mid-market rate on the same date. The gap — expressed in INR and as a percentage of the transaction — is your FX leakage per transaction. Aggregated across all transactions in a period, this gives you total FX leakage.

Should FX loss appear in P&L as an operating cost?

Accounting standards require it to appear somewhere in the P&L. But strategically, treating it as an operating cost creates the wrong incentives. Businesses that reframe it as unrealized revenue tend to invest more in optimizing it — and capture significantly more of what they earned.

Who should own FX optimization in an export business?

In well-run exporting businesses, FX optimization sits at the intersection of treasury and finance leadership. It is not purely an accounting function and should not be delegated to whoever processes payments. At USD 25k+/month volumes, it warrants dedicated oversight and quarterly review.

Does switching to a different payment platform reduce FX leakage?

It depends on the platform’s FX pricing model. Platforms that offer live interbank rate pricing with transparent spread disclosure allow you to measure and minimize leakage. Platforms that apply opaque rates (similar to traditional banks) simply replicate the same problem in a different wrapper. The key question to ask any provider: what rate do I get, how is it determined, and what is the spread over mid-market?

Leave a comment